F.A. RETAIL founder Fernanda Accorsi talks to TWM about the issues for tissues

Private Label (PL) is already a recognised brand in the market. If we consider the thousands of brands from all the retail chains worldwide as a single and solid brand, we realise that it became an important competitor, probably for almost all categories – of course with peculiarities among them. The sales of this new player have been increasing substantially during the past few years and the emerging countries point as a great opportunity for producers and exporters.

It is very important to mention the market share of private labels varies when we compare them across the globe. In the developed markets of North America, Europe and Australia, they are much more accepted as brands than in Asia, the Middle East, Africa and Latin America, where the quality of cheaper options is still questionable. The perceived value also varies widely from one category to another. Paper products are naturally perceived with little differentiation, and because it is usually considered a commodity, the generic brands in this case gain a larger space.

It is very important to mention the market share of private labels varies when we compare them across the globe. In the developed markets of North America, Europe and Australia, they are much more accepted as brands than in Asia, the Middle East, Africa and Latin America, where the quality of cheaper options is still questionable. The perceived value also varies widely from one category to another. Paper products are naturally perceived with little differentiation, and because it is usually considered a commodity, the generic brands in this case gain a larger space.

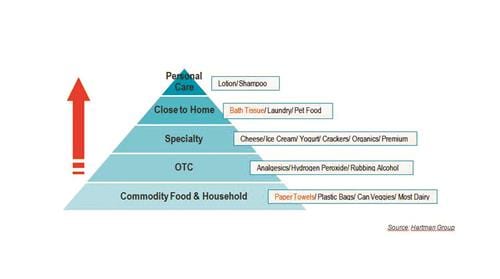

It is essential to understand that even within part of the same tissue segment, each category requires different purchase behaviours once they are addressed to different uses. Of course, we don’t buy toilet paper and facial tissue through the same insights we buy paper towels and napkins – and this statement is enough to explain why ‘personal care’ products present a higher degree of difficulty in switching from a name brand to a private one.

The issue for tissue

The purchase migration from national brands to supermarket store brands in the tissue segment is a reality and the level of sophistication gradually increases among the new players. It is not difficult to achieve the averages of softness, absorption and strength, especially today with the high number of manufactures, machines and new technologies. The issue is the ‘good value for money’ positioning that determines the costs and, consequently, the product quality. In developed markets (Switzerland and Spain, for example), with favourable perceptions about private labels, some SKUs already have quality comparable to national brands, and so consumers who expect a price advantage – in this segment it can be 30% less – also understand the similarity in attributes offered.

What is happening on the shelves?

It is in the POS (Point of Sales) where the private label movement shows its power, and this is where we see both sides performing their best strategies. Brand names at one side are investing time and effort in marketing to build recognised brands that can be purchased nationally (or internationally): new packaging, charismatic mascots and icons, (more) sustainable solutions, better embossing, value proposition, brand message, merchandising campaigns, three and four ply products. Brands that can react to price conflicts by offering small gifts and rewards or specific promotions to compensate their loyal shoppers.

On the other side we see the store brands bringing a timeless deal and a safe option for the neediest pockets. We also see higher investments on their marketing strategies and significant improvements on their SKUs – especially because some brands are produced by the same manufactures of the national brands and they have the know-how to reproduce quality patterns.

Facing this scenario, what is the best option? The answer is quite simple: both. There is no winner, they were made to survive together. For some retailers, PL is the main strategy and they have already replaced almost 100% of their paper portfolio with their own house brand, like the Spanish chain Mercadona – with its brand ‘Bosque Verde’. For the others, private labels can be the best option between the small and mid-sized brands and the fact of having an own label on the shelves can bring their customers closer to their business, improving the brand equity of the whole chain. My advice for these last retailers is: do it well because otherwise, if the clients notice that the quality is low, this will reflect on the company’s image and not only paper consumers will be disappointed – but all the customers.

Purchase insights: Every tissue category requires different purchase behaviour. Paper can be a commodity, but not always!

Finding the balance is a challenge

PL is not usually a direct competitor for the leading brand(s). Actually, the smartest way to show the consumers you have a good deal for them is by creating a healthy comparison between products and tiers – number of ply, softness, jumbo rolls, sizes, packs, etc. Keeping the main national brand in the assortment is a way of establishing a ‘quality standard’ for the chain and developing a correct ‘category management’ is also necessary in order to facilitate the purchase process to the shoppers. I have followed chains demanding that their brands should stand side by side with leading brands, not because of a common value proposition between them, but because of a forced positioning and this attitude does not help the client during his purchase experience.

Having the national brand is also profitable for the chains, once they usually get considerable contractual counterparts for having these big names on their shelves: they participate on big campaigns promoted by the brand, they negotiate extra investment for better exhibition, they negotiate secondary placement in the store (end caps, main entrance island, clip-strip exhibitions), they have a deal for damaged products and packaging and, in some countries, they still request a merchandising assistant from the industry to help in the POS with the ‘product replacement’ (in Latin America, for example). Name brands also bring customers to the store.

It is extremely relevant to think about the positioning of the chain in the market. Having a private paper brand can be an insightful strategy for big groups or franchising because of the scale of consumption and production, consequently. Discount formats and Cash &Carry stores are great opportunities for high-purchase categories like paper, and adding a PL may be interesting for the target – attention in addressing the right portfolio according to the store and the target profile.

While I was writing this article I tried to remember the first time I used (actually, the first time I bought) a tissue private label and I do not remember, which means that I did not notice much difference. And what about my current opinion: I buy PL sometimes and the quality of some SKUs is undeniable. If shoppers were submitted to an updated blind-test for tissue products, we would probably be surprised by the confusion among leader brands, small/mid-sized brands and private labels.

One last tip: transparent packing and a white and fluffy appearance are 50% of the success in this segment. Have you already noticed this?