By Fisher International’s Bill Burns

An area of high growth using value engineered conventional machines

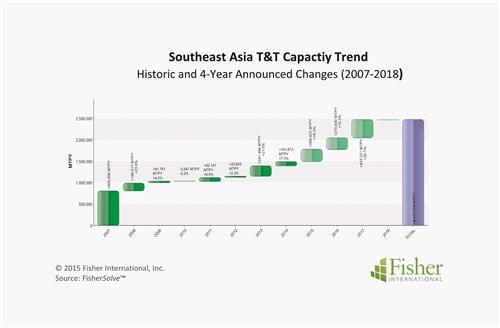

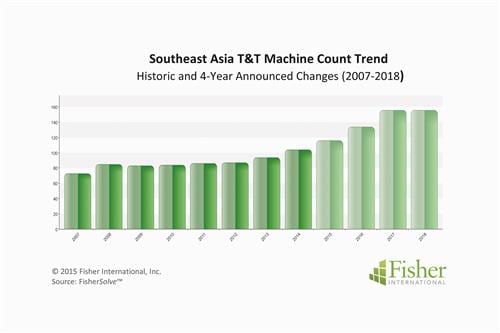

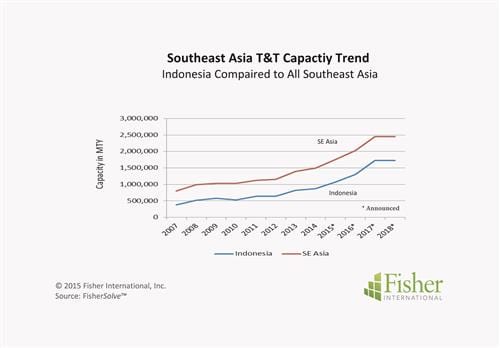

Southeast Asia’s Towel and Tissue (T&T) production had been experiencing modest but steady growth going into the 2013 – 2014 period. In 2014 several new lines were started or were under construction. Additional expansions were also announced, which, taken collectively, promise a greatly accelerated growth for the 2015 to 2018 period (Figure 1). The Cumulated Average Growth Rate (CAGR) for the period from 2007 through 2017 including the announced lines is a very respectable 10.6%. This compares solidly with the remainder of the rapidly expanding Asia Pacific region with 11.8% CAGR over the same period and a worldwide rate of less than 5%. This significant growth is, for the most part, coming from capital expansions with multiple new machines coming on line or being announced. As announced, Southeast Asia’s TM fleet will double by 2018 over the number of machines operating in 2007 (Figure 2), representing a three-fold growth in capacity over that timeframe.

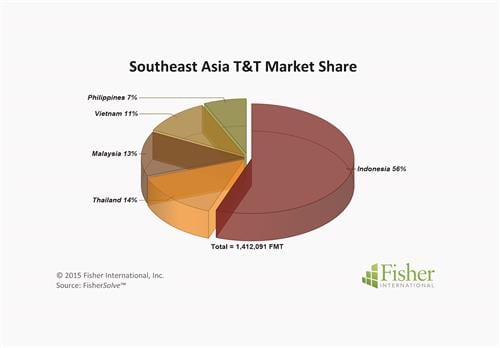

Some logical questions to ask concerning the Southeast Asian market would have to include: Where are all these machines located? When were the machines commissioned? What are the key dimensions of the machine base and new machines being planned? Breaking the market by country, it is clear that Indonesia has a commanding share of production in the region (Figure 3). With 56% of the market share, Indonesia has been and will continue to be at the centre of growth in the area.

‘Looking at the installed base of machines it is apparent that growth has come in surges. Presently, the area is experiencing another capacity increase.’

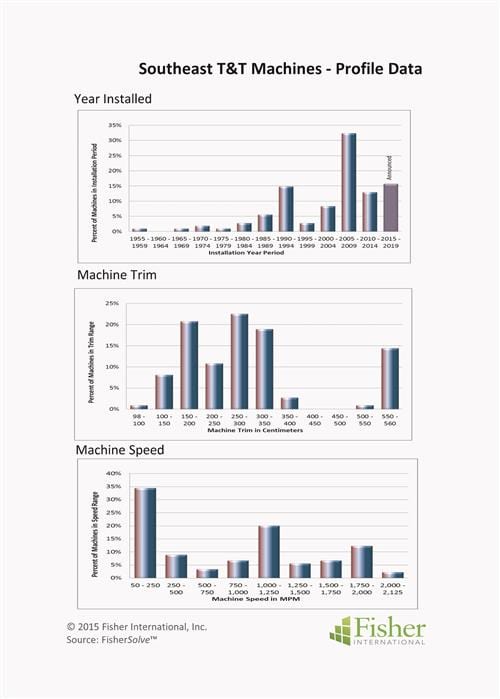

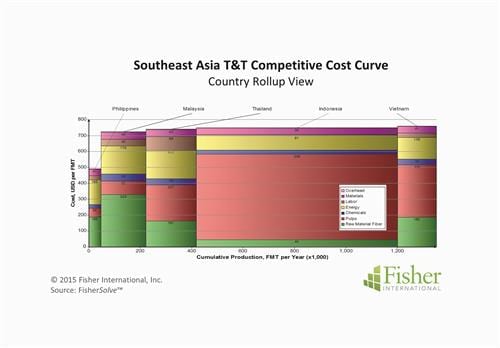

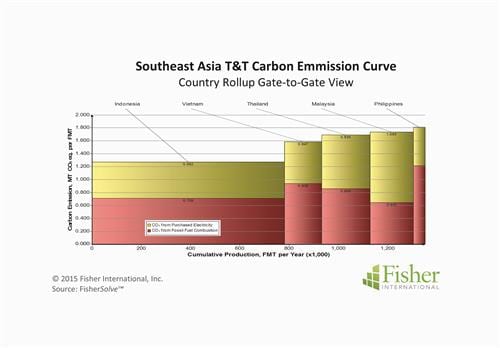

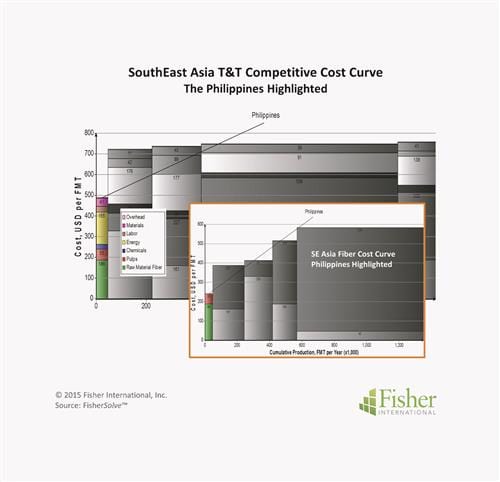

Looking at the installed base of machines it is apparent that growth has come in surges. The early 1990’s accounts for the first notable surge as about 15% of the machines are from that time period. In 2008 there was a very significant surge with some 30% of the machines coming on line in that time period. Presently, the area is experiencing another capacity increase. Announced capacity increases will account for yet another early-1990’s-like surge (Figure 4). The technology being installed is conventional paper machines of modest speed and trim. Only about 15% of the capacity is from machines five metres and greater. About half of the capacity in the area is coming from two to three-metre machines. Less than two-metre trim machines still hold a significant presence in the area (Figure 4). Like trim, speeds are also modest. While many of the recent additions will run in the 1,700 metres per minute range, there is a large installed base of lines operating at the low end of the speed range (Figure 4). Country to country, there is very little cost variance with one exception being the Philippines, which has a very advantageous cost profile compared to the remaining Southeast Asian countries. Looking at cost breakdown by category does reveal some very interesting differentiations among this tight cluster of nations that may be surprising: There is a remarkable difference in fibre cost from one country to the next. The largest producing country is heavily weighted to purchased market pulp where others are more integrated, resulting in a disadvantage for Indonesia. On the other hand, Indonesia has an advantage in energy and labour, offsetting the fibre cost. The Philippines hold the low-cost position for fibre which largely accounts for its overall low-cost position (Figure 5). Heightened focus on global climate change makes carbon footprint a potential competitive factor in the future. Public demand and government regulations can be expected to exert pressure to minimise a mill’s carbon footprint. Mitigation cost could be significant for some mills. For Southeast Asia, the mills using large amounts of coal and oil in their power and steam boilers will be most vulnerable. Although all countries have operations using some coal, Indonesia is in the best position while the country with the greatest exposure is the Philippines (Figure 6). Thus far, we have presented an overview of Southeast Asia’s T&T manufacturing environment with some comparisons between the countries in the region. The following profiles each of the five T&T producing countries in greater detail.

Indonesia

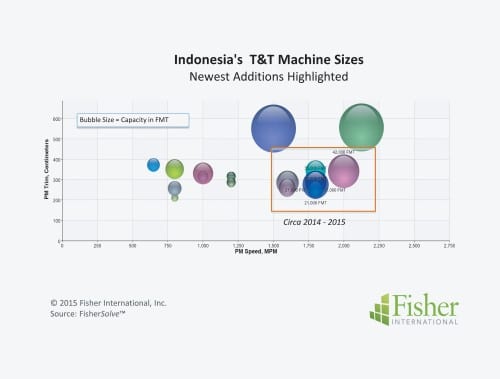

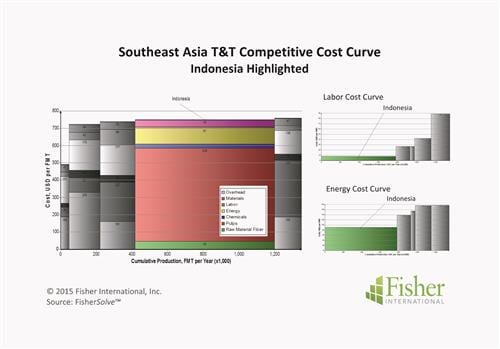

Indonesia’s T&T growth can be credited for much of the rapid expansion in Southeast Asia. With market share greater than 50% (Figure 3), it is clear that rapid expansion in this most populous country of the region, has placed Indonesia in a commanding position in the area. Taking announcements into consideration it appears that the trend will continue (Figure 7). Interestingly, Indonesia’s growth is being accomplished with narrow 2.5 – 3.0 metre class machines despite experience with wider, higher-capacity machines. Some of the recent machines (circa 2008) are designed to operate at modest rates of 1,200 metres per minute while the latest additions clock in at very respectable speeds approaching 2,000 metres per minute (Figure 8), suggesting a shift in strategy to higher producing assets. Indonesia’s overall cost position is comparable to most of the other Southeast Asian T&T producing countries (Figure 5). But unlike the other four, fibre represents the lion’s share of cost for Indonesia which relies heavily on the use of market pulps. Low labour and energy costs are offsetting some of the fibre cost disadvantage. Labour advantage is coming from both low wage rates and the ability to amortise the manning cost over high production capacity. Energy is driven by lower rates for both fuels and power when compared to the other Southeast Asian mills (Figure 9 side bars).

Thailand

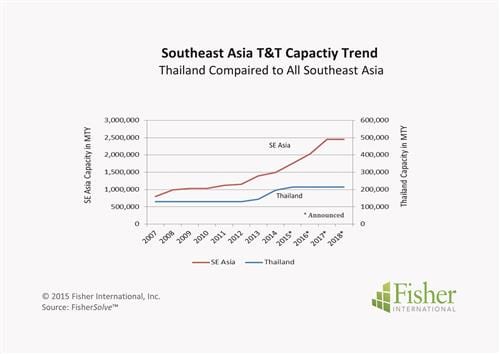

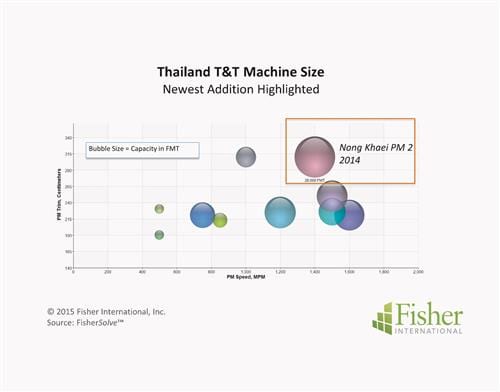

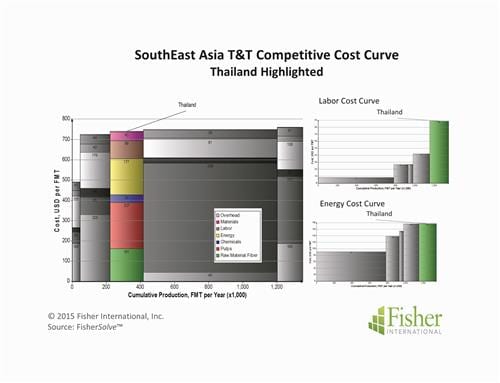

Thailand’s T&T industry has advanced at a Cumulative Average Growth Rate of 6.02% over the past eight years. This growth is, for the most part, coming from capital expansion with a new machine at the Nong Khai Mill and some productivity gains in recent years (Figure 10). With no announced capacity increases or decreases, future growth is somewhat in question at this time. Thailand currently holds a 14% share of Southeast Asia’s T&T capacity making it the second largest producing country (Figure 3); commensurate with its population but far behind Indonesia’s 56%. The paper machine base in Thailand is typical of the area with three metres or less in average width and operating speeds ranging from 450 to 1,600 metres per minute. The new machine, started in 2014, is big compared to other machines in the country. It trims out wider than most and at a speed within range of the fastest. Production rate of this new machine outpaces the remaining machines in the country (Figure 11). Thailand’s cost position is comparable to most other Southeast Asian countries (Figure 12). Fibre is typically the highest cost item and often the key differentiator throughout the region. For this cost class, Thailand is competitive. With labour and energy, Thailand is less competitive holding the high-cost position for the area in both categories (Figure 12 side bars).

Malaysia

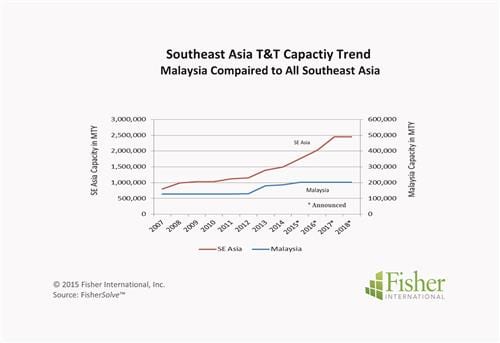

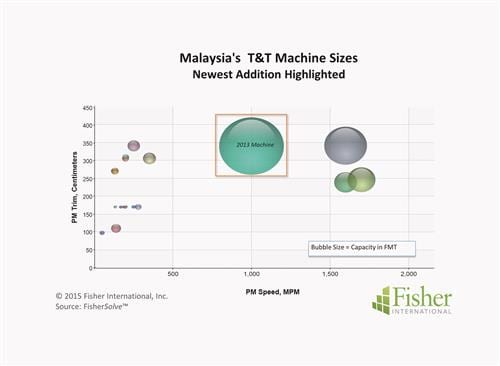

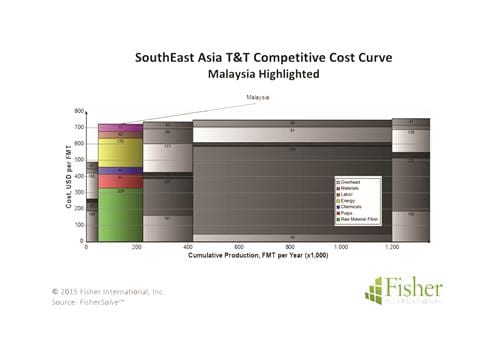

Malaysia’s T&T capacity trend is flat except for one new machine coming on line in 2013. There is some evidence of productivity gains as the new line is optimising. There is an announcement of another machine on the horizon but the timing is not clear. The trend curve for Malaysia is similar to Thailand adding to the overall Southeast Asian growth as a minor contributor (Figure 13). The future growth is somewhat in question with the uncertainty on timing for the one announced machine and no announced decreases or shutdowns on the horizon. Malaysia currently holds a 13% share of Southeast Asia’s T&T capacity (Figure 3) positioning it between Thailand’s 14% and Vietnam’s 11% even though Malaysia’s population is 1/2 and 1/3 of those countries respectively. The paper machine base in Malaysia is slightly on the higher side of three metre class machines and operating at speeds lower than most, ranging in the 250 to 1,600 metres per minute. The newest machine is a 3.5 metre machine running at 1,000 metres per minute (Figure 14). Malaysia’s cost position is second lowest on the cost curve but not too different from the other counties with the exception of the Philippines (Figure15). Fibre (all inclusive of purchased pulp and raw materials) is typically the highest cost item and often the key competitive factor throughout the region. For this cost class, Malaysia is on par with the other countries except for the Philippines and significantly advantaged to the capacity leader, Indonesia. In the other cost classes, Malaysia is neither in the high- nor low-cost position versus other countries with the exception of Indonesia where Malaysia is at clear disadvantage on energy cost.

Vietnam

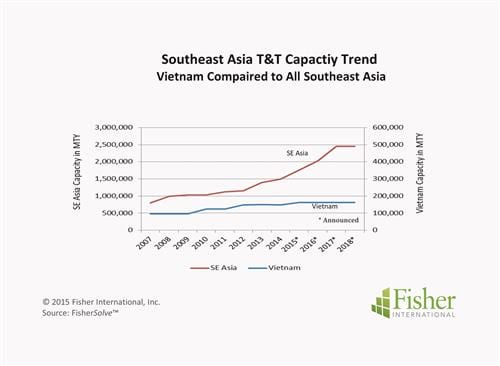

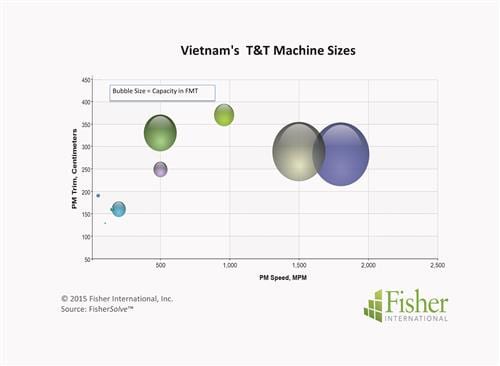

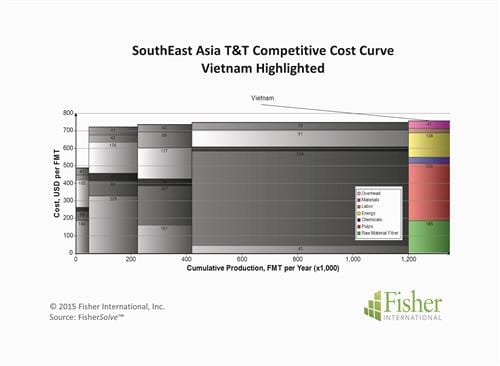

Vietnam’s T&T industry has advanced at a 6.67% CAGR over the past eight years. This growth is, for the most part, coming from capital expansion from three new machines added in 2009, 2010 and 2012 (Figure 16). With no further announced increases or decreases, capacity change is not anticipated at this time. Vietnam currently holds an 11% share of Southeast Asia’s T&T capacity making it the fourth largest producing country (Figure 3) and far behind Indonesia’s 56%. The paper machine base in Vietnam is typical of the area with two to three metre class machines and operating speeds ranging from less than 500 to 1,800 metres per minute. The two fastest machines are 2010 and 2012 vintages and combined, they represent the greatest capacity in the country (Figure 17). Vietnam’s overall cost position is highest, albeit by a small margin, against the other Southeast Asian countries (Figure 18). Fibre is typically the highest cost item and often the key differentiator throughout the region. For this cost class, Thailand is competitive with the largest producer, Indonesia, but higher-cost than the other three producing countries. In other cost classes, Vietnam is neither the high-cost nor the low-cost producer.

The Philippines

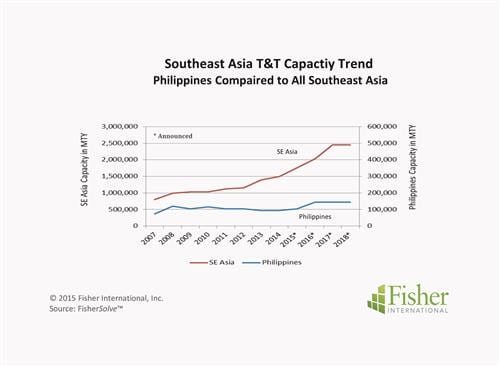

Philippine T&T capacity has been on a slight downward trend over the past seven years. There were two very modest machines added in 2008 and another in 2010; however the net number of machines has been falling over the period. The condition could be reversing for the near future as there are two machines announced for 2016. The trend curve for the Philippines is mostly flat obviously not following the trajectory of Southeast Asia overall or the growth of the major producing countries (Figure 19). The Philippines currently holds a 7% share of Southeast Asia’s T&T capacity making it the lowest producing country (Figure 3) though in terms of population, it is larger than Thailand. The paper machine base in the Philippines appears to be specified to support local markets. The machines are one and two metre in width and operate in the 200 to 500 metres per minute speed range. The highest capacity machine is a two metre machine operating at 500 metres per minute. The Philippines hold the low-cost position among the Southeast Asian countries. The nation has a clear cost advantage in fibre when combining pulp and raw materials (Figure 20). Looking at fibre alone, the Philippines has about $140 per metric tonne advantage over the closet competitive country and about $340 per metric tonne over the largest producing country, Indonesia. In the other cost classes, the Philippines is neither in the high- nor low-cost producer vis-à-vis the other countries. [box type=”info”] The source for market data and analysis in this article is FisherSolve™. About Fisher International, Inc. Fisher International supports the pulp and paper industry with business intelligence and management consulting. Fisher International’s powerful proprietary databases, analysis tools, and expert consultants are indispensable resources to the industry’s producers, suppliers, investors, and buyers worldwide. FisherSolve™ is the pulp and paper industry’s premier database and analytics resource. Complete and accurate, FisherSolve is unique in describing the assets and operations of every mill in the world (making 50 TPD or more), modeling the mass-energy balance of each, analyzing their production costs, predicting their economic viability, and providing a wealth of information necessary for strategic planning and implementation. FisherSolve is a product of Fisher International, Inc. For more information visit: www.fisheri.com or email [email protected] USA: +1-203-854-5390[/box]