By FOEX Indexes’ Lars Halén and Timo Teräs

NBSK pulp Europe

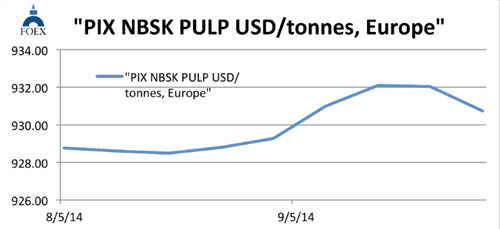

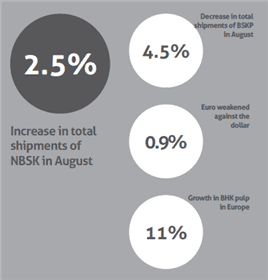

he August pulp data from PPPC came out better than expected for the hardwood pulp but the BSKP numbers were disappointing. Total shipments were up in August by 2.5%, y-o-y, which brought the cumulative eight month growth to 1.1%. In BSKP, shipments were down by nearly 4.5% for the month and now down by slightly more than 1% cumulatively. If the still positive fluff pulp data was removed from the BSKP total, pure paper grades softwood numbers would be even more negative. With the weak delivery data, market BSKP producer inventories moved up by two days including the seasonal adjustment and by three days without the adjustment. The market has remained firm in Europe but has showed some weakness in the other key consuming regions. Euro weakened again, this time by 0.9% against the US dollar. Our PIX NBSK index value headed further downwards, at least temporarily, as the index value retreated by 1.29 dollars, or by 0.14%, and closed at 930.74 USD/tonnes. When converting this dollar-value into the weakened euro with last Friday’s exchange rate, the benchmark moved further up by 5.82 euro, or by 0.80%, and the PIX NBSK index in euro ended at 731.02 EUR/tonnes.

BHK pulp Europe

In hardwood pulp, PPPC statistics showed an 11% growth in August, y-o-y. This brought the cumulative growth up to 3.8%. The earlier predicted impact of the abnormally high price gap between softwood and hardwood pulp is beginning to be seen in the consumption patterns. The approaching closure of Huelva and the idling of Old Town mill earlier in Maine help to absorb the growing volumes from the new lines in Brazil, Uruguay and China. Producer inventories in market BHKP were flat without the seasonal adjustment but came down by two days with the adjustment. Some producers have announced a 20 dollar price hike from 1 October, in addition to ENCE’s earlier announcement of a 20 dollar hike for all new business from September 15. Euro weakened by 0.9% against the US dollar. The PIX BHKP index value in Euro moved up again, this time by 5.74 euro, or by 1.02%, and landed at 569.29 EUR/ton. The PIX BHKP index value in dollars gained 55 US cents, or 0.08%, and closed at 724.82 USD/tonnes.

In hardwood pulp, PPPC statistics showed an 11% growth in August, y-o-y. This brought the cumulative growth up to 3.8%. The earlier predicted impact of the abnormally high price gap between softwood and hardwood pulp is beginning to be seen in the consumption patterns. The approaching closure of Huelva and the idling of Old Town mill earlier in Maine help to absorb the growing volumes from the new lines in Brazil, Uruguay and China. Producer inventories in market BHKP were flat without the seasonal adjustment but came down by two days with the adjustment. Some producers have announced a 20 dollar price hike from 1 October, in addition to ENCE’s earlier announcement of a 20 dollar hike for all new business from September 15. Euro weakened by 0.9% against the US dollar. The PIX BHKP index value in Euro moved up again, this time by 5.74 euro, or by 1.02%, and landed at 569.29 EUR/ton. The PIX BHKP index value in dollars gained 55 US cents, or 0.08%, and closed at 724.82 USD/tonnes.

Paper industry

Paper industry

Paper industry profitability remains sub-par, caused more by weak pricing than by higher costs. The number of recent mergers is not very high but capacity closures continue, especially in the graphic paper sector. Another recent trend has been the conversions of newsprint and other graphic paper capacity to another grade, typically brown packaging grades. Overcapacity has also led to some delays in building new capacity. This has been particularly clear in the tissue paper sector in China and other Asia.

Paper and paperboard shipment and production statistics over the first 6-8 months of the year confirm the earlier made predictions that the decline seen in the graphic paper sector over several years now will be slower in 2014 than in the previous two years. With that and with a slightly faster growth in the packaging sector, global paper and board production will grow more this year than in 2012 or 2013. There are big differences between the nations and regions, however. As an example, US paper and paperboard production was down by 1.9% over the first eight months.

During the first seven months, production in the CEPI countries was up by 0.1%. In Japan, the first six months ended up with an increase of 3.6% with even the paper sector up by 2.6% over 1st half 2013. Statistics from the developing countries are less regularly available but the numbers available point to a similar growth in 2014 to last year, depending, of course, on how the major correction in the Chinese statistics over 2013 data is treated in this comparison.

“‘In BSKP, shipments were down by nearly 4.5% for the month.”

Subscription – For access to the latest PIX Pulp and Paper index values and commentary, please subscribe to the “PIX Pulp and Paper Service” via the following link www.foex.fi/subscribe/

[box]

FOEX Indexes produces audited and trade-mark registered PIX price indices for certain pulp, paper packaging board, recovered paper and wood based bioenergy/biomass grades. The PIX price indices serve the market in a number of ways. They function as independent market reference prices, showing the price trend of the products in question. FOEX sells the right to banks and financial institutions to use the PIX indices for commercial purposes, while RISI Inc. has the exclusive re-selling rights for subscriptions to the PIX data and market information. Please enquire for subscriptions at [email protected] or via the following link www.foex.fi/subscribe/.

Tissue papers are produced either from virgin fibre, recovered fibre and various mixes of both, depending on the end product. High quality hygiene tissue products like medical tissue products, facial tissues, table napkins or other such household and sanitary products are often made exclusively or almost exclusively from virgin fibre pulp, whereas the share of recovered fibre typically increases in tissue products for a variety of end uses outside personal hygiene, such as kitchen towels or towels for garages or other such industrial production facilities etc. Providing PIX pulp price indices gives the paper producer and buyer insight in the price trends with a weekly frequency. PIX indices are used as market reference prices e.g.

- by banks or exchanges that offer price risk management services for pulp buyers and sellers

- by buyers and sellers of pulp or paper in their normal supply contracts

- companies who want to employ an independent market reference price for internal pricing (e.g. pulp mill – paper/paperboard mill, paperboard mill – box plant) through licensing the commercial use from FOEX.

In addition, our price indices are widely used in financial analysis, market research and other such needs by all kinds of parties linked directly or indirectly to forest product or wood-based bio-energy industries.

This way the companies have better tools to budget their cost or income structure and profitability, and may concentrate on their core businesses with less time spent on price negotiations, which tend to increase in these days as the planning span narrows in the wake of the short, quarterly business cycles and, nowadays, in most cases, monthly raw material pricing decisions.

[/box]