By RBC Capital’s markets analyst Paul Quinn

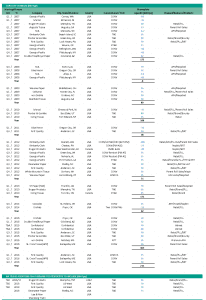

We believe that North American tissue margins could remain below historical levels for the next several years, particularly on the mid-to-low end of the quality spectrum. The industry is still absorbing the new capacity added in H2/12 and Q1/13, and will see another wave of capacity additions start-up in H2/15 and 2016 (see Fig 1 on page 60).

While some in the industry expect some older, higher-cost capacity to be shut as the new machines come online, we have not modelled in any unannounced closures. In addition, we suspect that a few of the future start-ups will be delayed in their start-up date but have not factored these into our supply-demand balance yet (Fig 2).

So the market looks congested ahead, but we know from experience that there will be movement in the current timetable to accommodate the capacity additions without material margin erosion.

US retail private label producer Clearwater Paper has reported increased price competition from branded/private label competitors throughout H1/14. In addition to increased promotional spending by branded producers (Clearwater cited one estimate that the branded producers’ ad spending was up 65% year-on-year in Q1/14), the industry also contended with lighter-than-expected order books in Q1/14 as retailer customers faced lower store traffic due to adverse weather conditions in January and February.

‘Clearwater Paper has reported increased price competition from branded/private label competitors throughout H1/14 … citing one estimate that the branded producers’ ad spending was up 65% year-on-year in Q1/14.’

While Q2 demand conditions improved, there was no shortage of branded promotional spending dollars seen. Many in the industry expect this “promotion rich” environment to be the new normal, as branded players fight the market share growth of private label producers.

On the Away-from-Home (AfH) side, we anticipate that a portion of the 8-10% AfH price hike announced by all major producers for July 2014 will be implemented. We view demand growth in the AfH market at 2-3% annually, with limited supply additions, which suggests that market conditions will improve in this smaller sub-sector of the market.

A potential issue on the supply side is the growth in parent roll production as producers with new machines that are unable to get enough orders for converted products are forced to sell increasing volumes into this low-margin end-market. Additional parent roll supply, typically lowers pricing to the point where independent converters produce for the AfH market.

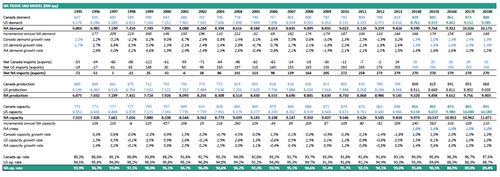

We anticipate lower operating rates in the medium term. We estimate demand growth at 1.6% per year, or 160,000tpy, largely driven by population growth with capacity creep at 95,000tpy.

‘Historically, paper and packaging producers only gain pricing power when operating rates are 95%+, and prices start to become ‘sloppy’ below 92% as pricing power then falls to the buyers.’

This implies that the market requires at least one new 70,000tpy machine annually in order to stay in balance. Factoring in likely capacity shuts, some in the industry believe that 2.5 new 70,000tpy machines per year are needed to meet rising demand. Unless additional capacity shuts are announced, we expect industry operating rates to decline to 91% in 2016. Historically, in paper and packaging businesses, producers only gain pricing power when operating rates are 95%+, and prices start to become ‘sloppy’ below 92% as pricing power then falls to the buyers.

Given additional capacity announ-cements for H2/15–H2/16 from Asia Pulp & Paper (two new 66,000tpy machines) and First Quality (two new TADs in addition to a planned ATMOS), we suspect that medium-term prices may be impacted by further capacity expansion (particularly if KP Tissue and Clearwater Paper end up adding additional TAD capacity).

‘RISI noted unconfirmed trade musings that an unnamed Chinese/Hong-Kong-based containerboard company is preparing an engineering study on the potential for placing up to eight new tissue machines in the US.’

In addition, Von Drehle is adding a new NTT machine in Q4/15 (35,000tpy). Further out, China’s Shandong Tralin has plans for a large $2 billion straw-pulp mill with integrated tissue production in Virginia (capacity unknown; construction to begin early 2016).

RISI also noted in April uncon-firmed trade musings that an un-named Chinese / Hong-Kong-based containerboard company (which we suspect is Lee & Man Paper) is preparing an engineering study on the potential for placing up to eight new tissue machines in the US.

Additionally, in March RISI noted talk in the trade that First Quality may be planning a third mill (with two machines) in the US West for 2017.

[box]TWM’s comprehensive Projects Survey 2014-2015 of global tissue companies’ attained and projected capacity expansion plans will be published in our January/February 2015 edition.[/box]