By FOEX Indexes’ Lars Halén and Timo Teräs

NBSK pulp Europe

The PPPC-statistics were fairly weak over July, but the August performance was again strong in softwood, especially taking into account the summer season, but remained subdued in hardwood. Total paper grade market pulp shipments were up in August by 5.6%, y-o-y, and now up by 3.7% cumulatively. For market BSKP, those changes were +9.5% and 3.4%, respectively. Shipments of all grades to Western Europe were up in August by 1.9%, y-o-y, but still down by 0.6% over the first eight months.

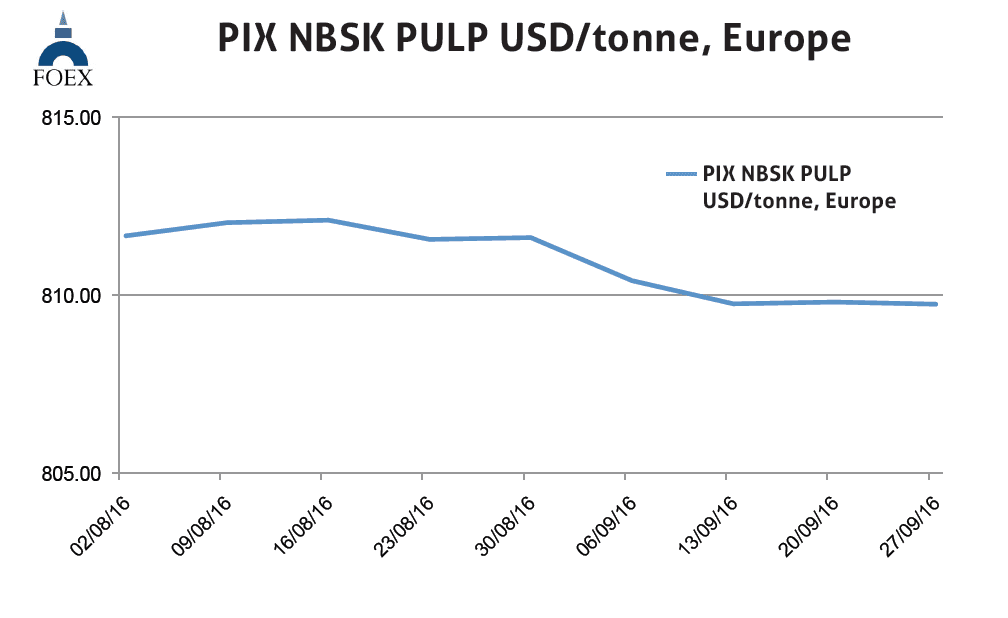

Market BSKP shipments to Europe showed a healthy 4.2% increase for the month, y-o-y, but a small retreat of 0.5% over the first eight months. Producer stocks for all grades were flat in the standard calculation but down by one day, seasonally adjusted, against July 2016. The softwood pulp stocks behaved exactly as the total. Our PIX NBSK index eased down marginally, i.e. by 6 cents, or by 0.01%, and closed at 809.75 USD/ton. US dollar strengthened against the Euro by 0.4% (weekly average, wk 38). With the weakening of the Euro against the US dollar, the benchmark value in euro, converted from the dollar value index with the average exchange rate of last week (wk 38), moved back up from last week by 2.78 euros, or by 0.39%, and the PIX NBSK index value in euro-terms settled at 723.64 EUR/ton.

BHK pulp Europe

In BHKP, the shipments to the global and European markets were not very strong in July and remained lacklustre in August. PPPC-statistics showed global market BHKP shipments up by just 0.9% for the month of August, y-o-y, but still up by 3.8% cumulatively over January-August. Hardwood pulp shipments to Europe were again slightly down. In August, the retreat was 0.4%, y-o-y, and over the first eight months, shipments were down by 0.9%. Increasing downtime helped the hardwood pulp producer stocks which were flat without seasonal adjustment but, seasonally adjusted, came down by two days from end July 2016. Against August 2015, those stocks were still up, seasonally adjusted, by five days. Port stocks in Europe moved up in August by about 50 000 tons for all grades. This was a much smaller increase than in August 2015 and the total stock

level of 1.25 million tons, while high, was below port stocks at the end of August 2015. Our PIX BHKP index value retreated again, this time by 51 cents, or by 0.08 %, and closed at 661.64 USD/ton. In week 38, the value of Euro depreciated by 0.4% against the US dollar (weekly average). When converting the USD value of the BHKP benchmark into the moderately weakened Euro, the PIX BHKP index value in Euro moved up by 1.86 euro, or by 0.32%, and closed at 591.28 EUR/ton.

Paper industry – (Sep. 13, 2016)

The first half year paper and paperboard production numbers have now been published by most of the key countries and regions. In graphic papers, the global supply (and demand) continue to sink. Over the first six months of 2016 production was down in CEPI-countries by 3.7%, in USA by 4.5%, in Canada by 3.8% in Japan by 1.3% and in South Korea by 2.1%. Brazil showed a growth of 1.0%. In tissue, production grew in all key countries, except for South Korea. E.g. in CEPI-countries, the growth was 2.5%, in the US 0.5% but in Japan as much as 5.0%.

Sep.27, 2016): The August data on the paper and board industry shipments looks better than what it really has been, due to two more shipping days in August 2016, compared to August 2015. Helped by this high number of working days, e.g. the North American printing and writing paper statistics (by PPPC) show a 2% rise in total shipments, y-o-y. The cumulative numbers are still down by 2.5% compared to the January-August volume shipped in 2015. Woodfree papers did this time clearly better than the wood-containing ones. In uncoated free sheet, the largest grade, the gain in August was 3.3% and also the cumulative number over the first eight months was marginally positive at 0.2%.

In Europe, no data on paper industry production or delivery volumes over August is at our disposal at the time of writing this report. Even if some pick-up has been reported now in September, most of the August data is likely to come out fairly weak, even seasonally adjusted. The order books were short in August and prices were under pressure in many grades. In container boards, July numbers showed a 4.4% y-o-y decline in the European total, much worse than the cumulative retreat, which is still nearly 2.5%. Recycled paper based case-making material producers have been repeatedly disappointed through the summer in their efforts to raise prices. In North America, some of the packaging sector price increase attempts seem to have more wind under their wings.

About FOEX

Subscription: For access to the latest PIX Pulp and Paper index values and commentary, please subscribe to the “PIX Pulp and Paper Service” via the following link www.foex.fi/subscribe/

FOEX Indexes Ltd produces audited and trade-mark registered PIX price indices for certain pulp, paper packaging board, recovered paper and wood based bioenergy/biomass grades. The PIX price indices serve the market in a number of ways. They function as independent market reference prices, showing

the price trend of the products in question. FOEX sells the right to banks and financial institutions to use the PIX indices for commercial purposes, while RISI Inc. has the exclusive re-selling rights for subscriptions to the PIX data and market information. Please enquire for subscriptions at [email protected] or via the following link www.foex.fi/subscribe/.

Tissue papers are produced either from virgin fibre, recovered fibre and various mixes of both, depending on the end product. High quality hygiene tissue products like medical tissue products, facial tissues, table napkins or other such household and sanitary products are often made exclusively or almost exclusively from virgin fibre pulp, whereas the share of recovered fibre typically increases in tissue products for a variety of end uses outside personal hygiene, such as kitchen towels or towels for garages or other such industrial production facilities etc. Providing PIX pulp price indices gives the paper producer and buyer insight in the price trends with a weekly frequency. PIX indices are used as market reference prices e.g.

– by banks or exchanges that offer price risk management services for pulp buyers and sellers

– by buyers and sellers of pulp or paper in their normal supply contracts

– companies who want to employ an independent market reference price for internal pricing (e.g. pulp mill – paper/paperboard mill, paperboard mill – box plant) through licensing the commercial use from FOEX.

In addition, our price indices are widely used in financial analysis, market research and other such needs by all kinds of parties linked directly or indirectly to forest product or wood-based bio-energy industries.

This way the companies have better tools to budget their cost or income structure and profitability, and may concentrate on their core businesses with less time spent on price negotiations, which tend to increase in these days as the planning span narrows in the wake of the short, quarterly business cycles and, nowadays, in most cases, monthly raw material pricing decisions.