Following their retailer customers, tissue producers expand to new regions, provide the segments and qualities requested, and step up to meet environmental demands. A TW report.

By Pirkko Petäjä, Pöyry Management Consulting

RETAILERS IMPACT THE GEOGRAPHIC SPREAD OF PRODUCERS

Often the geographic spread of tissue producers originates from the retailer requirements. Many, especially private label producers, have followed retailers to new markets. Producers have had to match the retailers in size, be large enough and also be present in several countries in order to serve their retailer clients. Relationship with retailers, large scale and capability to supply large volumes in several locations, creates an advantage compared to small local competitors. The expansion of Italian companies in the 1990s and 2000s to several European countries has followed this pattern. This has shaped the whole European tissue supply.

RETAIL STRUCTURE AND PENETRATION OF THE LARGE RETAILER GROUPS OFTEN DETERMINES PRIVATE LABEL AND BRANDED SHARES

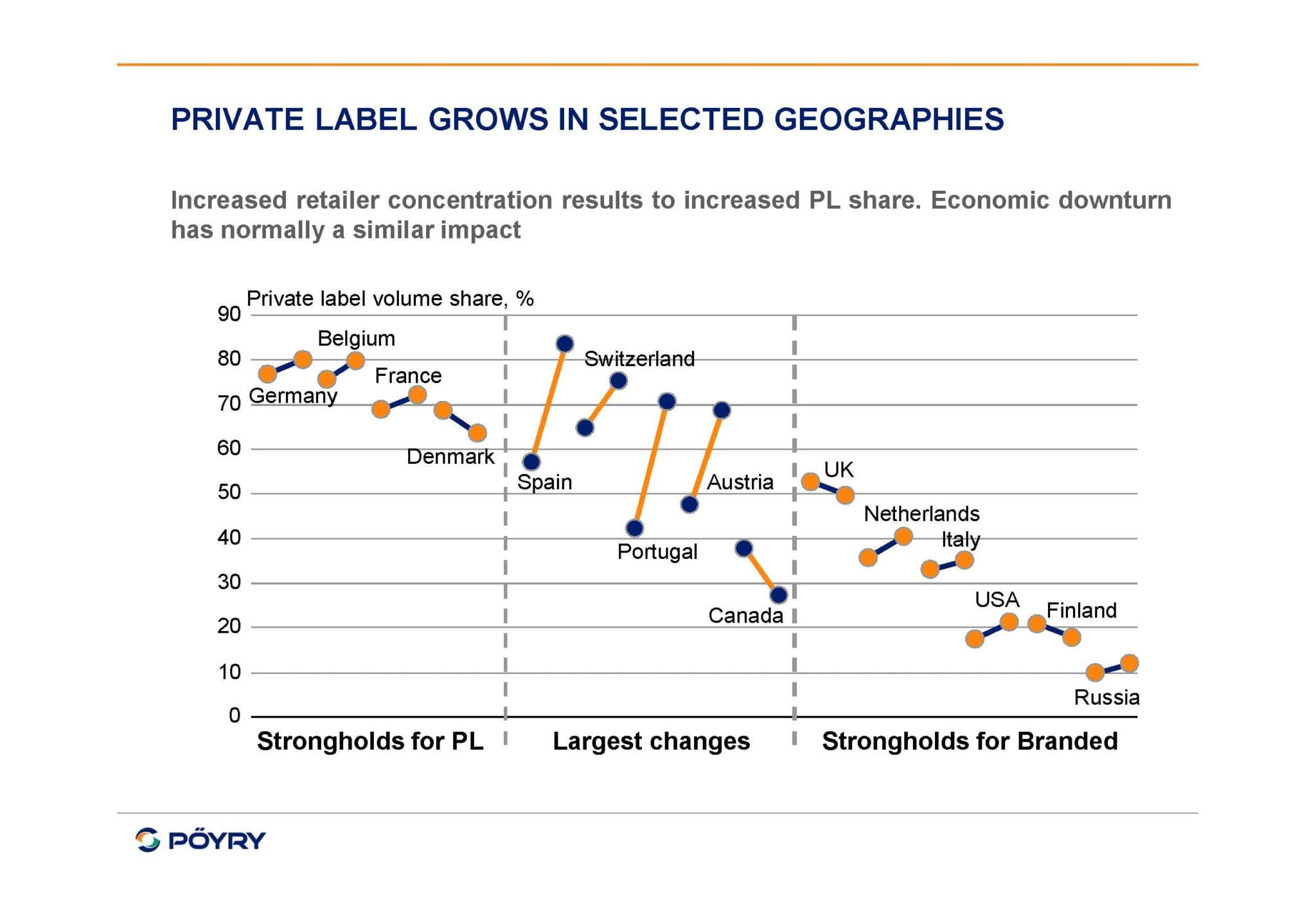

The retail structure is often a good indicator of the tissue market’s developments. Retailer structure, concentration, the number of retailers and what types are present in a market determine the market extensively. If major retailer chains that typically drive their own brands (Lidl, Aldi) have a significant share, this enhances the high private label share in a region. If hypermarket chains and discount stores are dominant (and also if there is an economic downturn) this means the focus is on prices and consequently often to private label, or at least away from the most exclusive

brands.

In countries where the retailer structure is fragmented, there is often more room for manufacturer brands. The Italian tissue market is primarily branded. In Italy distributors also quite commonly serve the smaller shops and manufacturer brands are therefore dominant. The leading Italian producers are also quite strong and capable of keeping the business in their own hands. If the dominant retail chains are purely

local like for instance in Nordic countries, especially Finland, the importance of private labels has not reached the same level as when the multinational chains rule.

However, retail structure is not the only factor impacting the market segmentation. With similar retailer structure private label share can be different as some other issues overcome the retailer concentration impact. In markets like the UK the presence and efforts of strong multinational tissue brand owners (e.g. Kimberly – Clark and Procter & Gamble) has shaped the market to resemble somewhat the market in the US with the strong brand focus. Even the popularity of products/categories follows these producers and also in this respect the UK tissue market is close to the US market; boxed facial tissue is more popular than hankies. In most other Western European countries facial tissue in boxes has

not been able to maintain great volumes.

Typically in smaller markets, a similar traditional presence and market dominance not of the multinational giants but the national players/brands creates a brand focus. Such examples are Slovenia with Paloma and Finland with former G-P and Metsä-Tissue. Russia is a branded tissue market. The success of brands is, however, restricted by the average low quality of products that the majority of the population can afford. The future development following the rapid progress of domestic and international retailer chains and the increase of disposable income, is, however, not expected to essentially change the segment structure; Russian buyers typically like brands and growth concentrates on

major cities where the buyers can better afford both the international and national brands.

RETAIL DETERMINES EVEN THE MARKET PLAYERS

The negotiating power of tissue brand owners has not been strong enough in the Western European markets to create the similar brand dominance in supply as seen in the US. Even the strong efforts of the main brand owners to gain market share in the key European markets (e.g. Procter &

Gamble) have succeeded only partially. This is the reason for Procter & Gamble’s withdrawal from the European tissue business and the same applies to Georgia Pacific and Kimberly Clark’s withdrawal from the consumer business in selected markets (Poland and Germany); the retailer labels are too strong and it is not possible to improve the margins to the levels the brand producers are typically used to.

“Retail shapes the tissue industry as it determines the suppliers’ geographic spread, requirements for their minimum size and impacts the brand and private label segmentation.”

The European tissue consolidation is also the consequence of retailer impact as actually the retailers have forced the players to organic growth and acquisitions to give them required geographic presence and enabling them to be strong enough to cope with the retailer groups. Consolidation in Europe is going to continue; the large groups clearly show a more stable performance due to the strengthened position and increased negotiating power. We are going to see further consolidation moves, as there is the danger that the smaller players end up as second tier producers squeezed by the oligopolistic market leaders.

ROLE OF CONSUMERS

The end consumers show what they want with their buying decisions. Typically the trend is towards higher quality in all segments throughout the markets. Hardly anywhere is lower quality a long term trend, even if it can be temporarily gaining share. Private label quality is approaching the brand quality; even TAD is entering the private label segment.

Economics, the level of disposable income and the state in the economic cycle are the strongest indicators of consumer behavior. The impact of the economic downturn can clearly be seen in consumers’ turning to cheaper products, often private label, and lower quality. The volumes seldom decrease due to the downturn, as tissue is seen as a necessity and nobody cuts down the usage for economic reasons, although one can of course choose cheaper quality. The strong increase of private label shares due to the economic downturn has been clearly seen for instance in Spain and the Iberian Peninsula in general.

The consumer decision is primarily economic. They can for instance respect the environmental argument but they are not willing to pay for it. Consumers choose the ‘environmental’ alternative if the price is the same, but no meaningful premium will be paid for any such attributes. Several consumer surveys indicate that although the majority of consumers claim that raw materials influence their buying decision, only 20% are willing to pay for ‘eco friendliness’. Some tissue producers believe that consumers might be willing to pay for these attributes in the future; however, nobody believes this is possible in an economic downturn, but maybe in a better economic climate.

The price is always somehow behind the consumers’ buying decision. New innovations and features may fascinate temporarily, but not at any price. The same is true with tissue suppliers; their decisions are finally always economic – if the recovered fibre content or environmentally-certified fibre or Bamboo is not paid by the final customer it will not be a sustaining feature. Only the NGO’s and retailers can afford to be idealistic

and require something that at the end of the day is paid for by somebody else. Therefore, the environmental attributes and labeling are also primarily requested by those groups. In certain regions, especially in Germany, some environmental requirements are a must as the retailers do not offer anything else; the retailers finally shape the tissue offerings. If the trade was in the hands of small fragmented players, quite different forces would rule and the markets would be a long way from the currently ruling of extensive environmental labeling.

CAN THE MARKETS BE ACTIVELY IMPACTED OR SHAPED?

The impact of the retailer on the tissue industry is most likely to be a consequence of their existence and position. Different types of campaigns to boost a brand for instance have not proven to have a permanent impact because after the campaign the market goes back to normal.

European tissue producers are still trying to shape the market towards more branded products; that is the announced intention of SCA’s consolidation moves and this target is possibly reached when combining P&G and G-P’s brand power to SCA’s.

Consumers make rational choices. High quality is the trend and there will always be a premium segment where price is not decisive. TAD and multiply defend their position and there will be interest in similar properties and functionality, the more affordable the wider the interest. In a normal economic situation the trend is gradually moving to higher qualities and coming down in quality is not possible without repositioning and significantly lower prices. Higher quality increases prices and volumes and is therefore in the interest of producers. Large diameter maxi rolls, paper designed for certain purpose, etc, are all good selling points but the price must always be balanced with the purchasing power.

SUMMARY

Retail shapes the tissue industry as it determines the suppliers’ geographic spread, requirements for their minimum size and impacts the brand and private label segmentation. Retail has even impacted market players; the negotiation power of the brand owners has not been enough in the European tissue markets and consequently the large multinational brand players have exited.

The current European tissue consolidation is driven by the search for the market power and it is shaping the European tissue supply towards an oligopolistic market. The consolidation is expected to continue.

The final consumer makes rational, often economically driven buying decisions. They are usually not ready to pay for environmental attributes, labelling or certification, even if they may prefer these qualities if the price is the same. Retailers cannot have much impact on the market by active campaigns, but they can influence the decision to have environmentally certified products from their suppliers.

PÖyry Management Consulting is the leading advisor to players within the global Paper, Pulp, Packaging and Hygiene sector

w. www.poyry.com