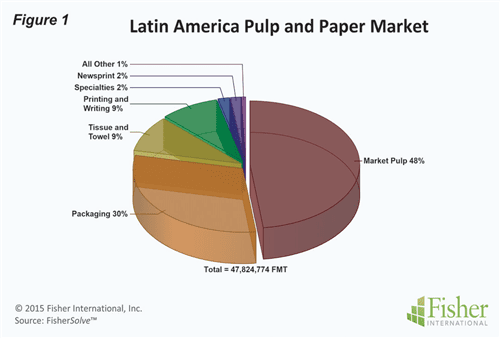

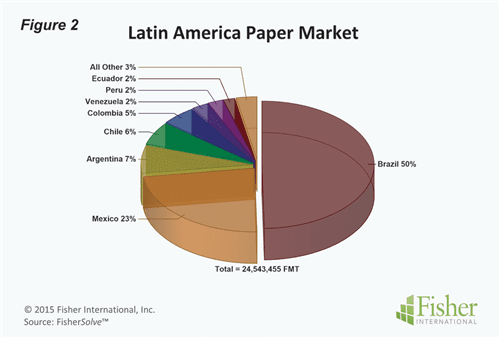

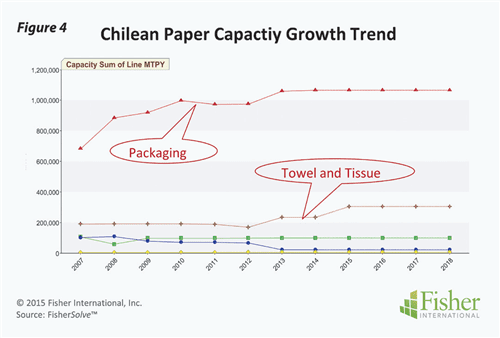

Chile is the number three pulp and paper producing country in a Latin American market that is heavily weighted to pulp production. Nearly half of the 48M FMT pulp and paper market in Latin America is market pulp production (Figure 1). Taking market pulp out of the picture and looking at paper production exclusively, the market is about 24.5M FMT, dominated by Brazil with a 50% share while Chile is fourth largest producer with a 6% market share (Figure 2). Overall, the Latin American paper market has been growing slowly but steady over the past seven years. Announced increases suggest the growth trend will continue for several years to come (Figure 3). Looking at Chile, we see growth in two segments. Packaging has been growing at a very fast rate outpacing all other grades. Towel and Tissue (T&T) growth has kicked up in the last couple of years and there is an announced increase in 2015 (Figure 4).

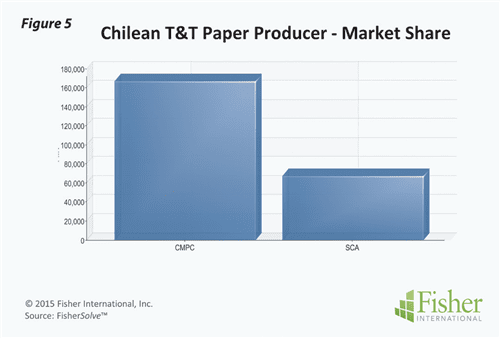

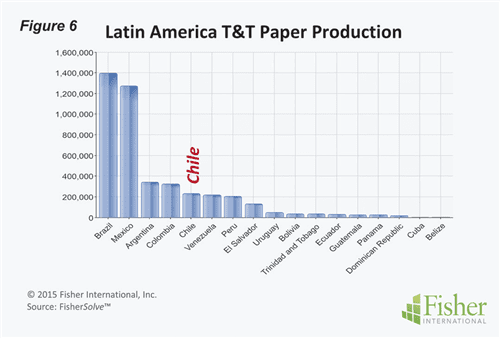

The T&T market in Chile is shared by two companies CMPC and SCA (Figure 5). These two companies combined make Chile the fifth largest producer in Latin America. Of course, that statement is somewhat misleading as two countries, Brazil and Mexico, dominate the market with production levels three to four times the next largest producing countries (Figure 6).

‘‘The Chilean T&T market is shared by CMPC and SCA. Combined, these two companies make Chile the fifth largest producer in Latin America.’’

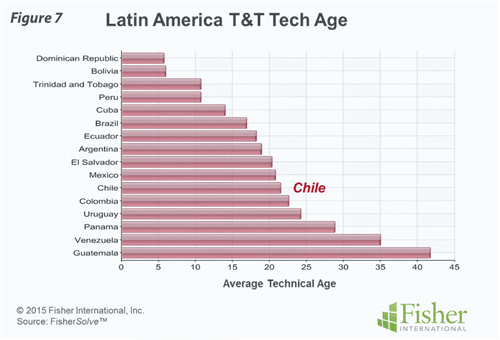

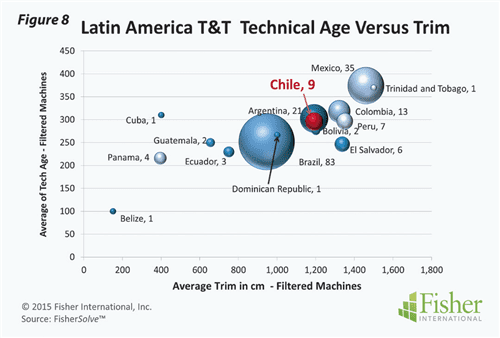

Looking at competitive factors beyond overall capacity we see that the machines in Chile are technically older than most of those in other countries in the region (Figure 7). Plotting the number of machines in a bubble chart against technical age and trim we see that Chile’s nine machines are above average age and at average for trim (Figure 8).

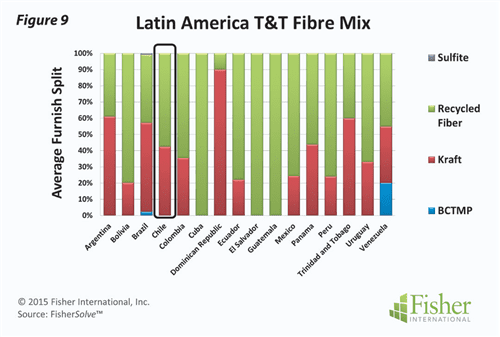

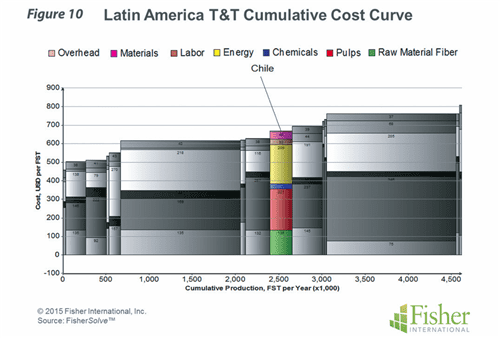

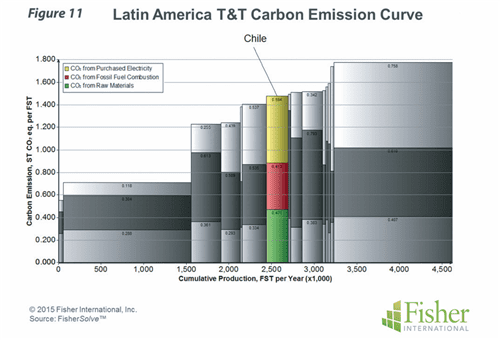

Competitive cost position tends to be driven by fibre choices. Chile’s fibre sourcing is not too dissimilar from the largest producers with 50% +/- Recycled Fibre and the remaining being Kraft pulp (Figure 9). Viewed on a Latin American T&T cumulative cost curve, Chile is in the middle of the pack (Figure 10). As expected, countries with higher dependency on costly market pulp have high cost and those with more self-sufficiency in recycled or integrated pulp have lower cost. Cost competitiveness must be considered within the context of what could be costly due to regulations in the future. Carbon emissions have the potential to impact cost positions and disrupt the current balance in the future. When carbon emissions for the countries in the region are modeled, Chile falls in the center (Figure 11) with a significant player holding a considerably lower emissions position.

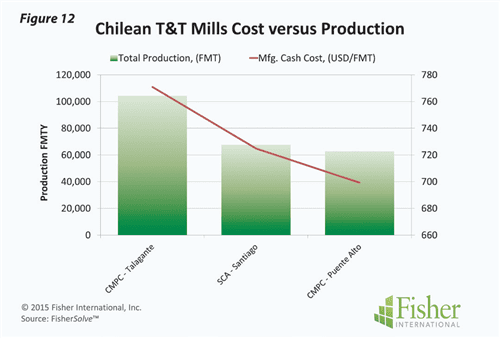

In the end, competitiveness in T&T tends to be local. Typically, the company or mill with the best cost position, the right product performance, and adequate capacity to meet the needs of its market should have a strong market position. Assuming all competitors make comparable quality products that meet end users’ needs, the low cost producer should command the market. In Chile the reverse appears to be the case. The low-cost mill has the lowest capacity while the largest mill (in terms of T&T production) is also the highest cost-per-ton producer (Figure 12).

The source for market data and analysis in this article is FisherSolve™. Data tables behind Figures 1 – 12 can be obtained from Fisher International. E-mail requests to [email protected].

About Fisher International, Inc.

Fisher International has supported the pulp and paper industry for over 25 years with business intelligence and management consulting. Fisher International’s powerful proprietary databases, analysis tools, and expert consultants are indispensable resources to the industry’s producers, suppliers, investors, and buyers worldwide.FisherSolve™ is the pulp and paper industry’s premier database and analysis tool. Complete and accurate, FisherSolve is unique in describing the assets and operations of every mill in the world (making 50 TPD or more), modeling the mass-energy balance of each, analyzing their production costs, predicting their economic viability, and providing a wealth of information necessary for strategic planning and implementation. FisherSolve is a product of Fisher International, Inc. For more information visit: www.fisheri.com or email [email protected] USA: +1-203-854-5390.