By Euromonitor Research Analyst, Ahmed Bakr

With the recent relaxation of sanctions, the Iranian economy is expected to experience a more stable situation in 2016. Real GDP is expected to grow by 4% in 2016, up from 2% the year before, and with the elimination of certain sanctions boosting oil production within the country, driving overall growth further. Moreover, it is now easier for companies to invest in and manage their procurement portfolios due to changes in government legislation.

But other factors also bode well for investors. Iran is in the midst of a moderate population boom, with its total population reaching nearly 80 million in 2015, having increased by about 13 million since 2000. In addition, it has a young population, with a median age of 29.6 years in 2015. The young are typically seen to be more progressive in their views and are willing to try new things. As the population increases, many Iranians are also choosing to live in cities. According to the Iranian Statistical Centre, the proportion of the country’s households located in urban areas increased to 73% in 2015, up from 68% in 2006, bringing an increase in modern retailing along with it.

The retail tissue market in Iran

As with other consumer goods markets, the retail tissue market is expected to benefit from these positive signs, prompting investment in the market and the appearance of more international brands. It is expected that as the Iranian market continues to develop, consumer awareness of tissue and hygiene products will also grow, due to increasing hygiene standards and consumer perception of these products. With middle-class consumers gaining higher purchasing power due to a rise in disposable income, tissue products are also becoming part of the daily shopping cart. The market registered 5% growth in volume terms (tonnes) in 2015 over the previous year, and is expected to remain healthy over the coming five years, with a volume CAGR of 6% through 2020.

As a further sign of this growth, Iran has witnessed a wave of investment in this sector over the past few years, including new tissue paper mills and machinery in 2015 and 2016, such as Aryan Cellulose Sanaat’s new mill with an estimated capacity of 35,000tpy and new machines at Zarrin Barge Persia and Narmeh Paper Industries. This is causing an expansion in the country’s tissue volume. Some other tissue mills are expected to enter the market by the end of 2016, including, most recently, the paper mill developed by Arian Cellulosa Sanat in Eshtehard, with an estimated capacity of 35,000 tonnes per year.

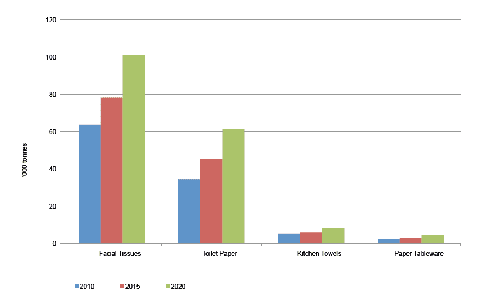

Traditionally, tissue consumption in Iran centred on two main categories: facial tissue and toilet paper. These categories accounted for 59% and 34% of volume sales, respectively, within the retail tissue market in 2015. Price and availability continues to play a crucial role in purchasing decisions. As such, the market for retail tissue in Iran is showing aggressive competition. For example, leading company Pars Crepe Co depends upon its long-standing presence in the country and in-store promotional activities to drive higher volume growth. Equally, as modern retailing gains further ground in the country, companies are making their products available at both independent grocery retailers and hypermarkets/supermarkets. This is creating stronger visibility for tissue products and, along with relatively low unit prices, is stimulating increased demand.

Toilet paper is on a roll

Toilet paper is also experiencing healthy volume growth, reaching 6% in 2015. Traditionally, the most widely found type of toilet in Iran has been the squat toilet, with water typically used for cleaning, not requiring toilet paper. However, due to urbanisation and greater influence from the West, this tradition has changed over recent years. Flush toilets have increased in popularity, especially within urban and affluent areas, positively affecting sales of toilet paper.

The majority of toilet paper in the market is offered by domestic brands, produced locally. There is very minimal difference when it comes to unit prices among different brands. Promotions and availability are the major factors on which companies compete. Currently, Pars Crepe Co is the leading toilet paper company, with a 27% value share, followed by Khorasan Paper Products Co, on 18%. The rest of the market is divided amongst other domestic players, all of which focus on economy toilet paper. Most consumers prefer buying toilet paper to meet their immediate needs to save money rather than buying bigger pack sizes and paying more – even if in the long run these larger pack sizes offer more value for money. Double rolls in flexible plastic packaging is the most common pack size and format in Iran.

Facial tissue also seeing positive growth

Facial tissues also continues to see positive growth in Iran, increasing by 5% in volume terms in 2015. Boxed facial tissues continues to account for the bulk of this category, at around 98%. The improvements in the standard of living, as well as the wider availability of these products in both traditional and modern retailers, continues to drive growth. Moreover, the relatively low unit price for these products makes them a popular purchase.

The increase in distribution has affected other categories within retail tissue as well, for example kitchen towels and napkins. These categories registered the fastest volume growth in 2015, at 7% and 9%, respectively. Growing from a low base, kitchen towels and napkins are now widely available in hypermarkets and supermarkets, making this a major driver of their growth. Iranian consumers, especially those in the middle and upper class, are learning about the multiple benefits of such products.

Innovation and competition to further drive the category

The Iranian retail tissue market is expected to continue its strong performance over the forecast period. It is also expected to see enhanced marketing activities by key players, which will continue to drive a relatively low unit price. Moreover, further manufacturing investments are expected to raise the country’s capacity for producing these products, bringing an increase in availability and competitiveness. As such, key players will shift priorities to invest more in research and development and focus on innovation in order to differentiate their products in the market. New products focusing on quality will also continue to appear, providing a more premium offer for middle- and upper-class consumers.