Somnath Ray, Principal, AFRY Management Consulting, urges the industry to assess the risk of potential disruption to traditional international and regional logistics.

The global tissue market has experienced a consistent upward trend since the 1920s when tissue papers started to receive widespread adoption. This enduring growth can be attributed to several factors, such as increasing disposable incomes and rising healthcare expenditures, which constitute a solid foundation for growth. The tissue market also weathered several challenges to demand from salvos such as market downturns, market stagnation due to population growth changes in certain regions, and much more. And recently, like most of the paper and paperboard segment, the tissue paper segment also woke up in 2025 with headwinds from tariffs and embargoes.

Unlike any other paper commodity, the general wisdom is that tissue paper doesn’t travel far, so the headwinds should have a limited impact. However, I was subtly reminded of an interesting conversation on a recent trip to South China, where I had the chance to visit several tissue converters that produce different private labels and other brands. Many of these enterprising operations procured jumbo rolls and converted tissue per the customers’ needs in domestic and international markets. We had some interesting discussions, and past the usual talk about business dynamics and market growth, several strategic questions cropped up.

The general theme was the worry about disruption of international trade due to upcoming changes in governments and their ideologies – in short, the possibility of bringing back some of the tariffs and trade embargoes we saw a few years back. This made me wonder if there is an international market supply or a regional supply for tissue paper, and which one is more dominant so we can gauge the exposure from tariffs and trade embargoes.

As a hypothesis to investigate further, we saw two possible trade models – jumbo reel production in one region to be converted in the destination region, and international direct-to-consumer supply through either e-commerce portals or other supply channels. The first is a tried and tested model, which several Asia-based producers are increasingly pushing forward through strong relations with converters and brand development. However, the second model is relatively new and has been shipping products promoting “direct to consumer” low-cost models. We see widespread discussion and scrutiny of these platforms as they have had explosive growth in the US, bypassing de minimis requirements. Also, this was the one I mentioned that was discussed more during the recent trip.

The dominant trade model in the tissue paper market depends on several elements. Generally, the tissue paper market is a high-volume, low-cost production model focused on economies of scale, efficient distribution networks, and consistent quality control. Major players like Kimberly-Clark and Essity rely on brand recognition and product differentiation to maintain market leadership. Similarly, several Asia-based producers have also developed their own brands over time.

These key elements of this business model impact in varying degrees:

- Production and converting: Producing tissue paper (jumbo rolls) at a single facility to benefit from cost reductions through bulk purchasing raw materials and optimised production processes. And then ship them to the destination market to be converted into finished products. Another approach has been to focus only on one market with production to convert at one location. So, to reap the most benefit it makes most sense to be close to key demand markets.

- Vertical integration: Controlling multiple stages of the production process, from pulp sourcing to packaging. Also, often having their own dedicated converters or partner converters on long-term contracts. This is done at varying levels to maintain brand quality, streamline operations, and reduce costs. Investing in all stages of the production process is a decision based on location, access to fibre and investment appetite topic.

- Distribution network: Maintaining a robust distribution network to reach a vast customer base through supermarkets, convenience stores, and wholesale channels. Also other channels as the fast growing ecommerce market.

Other elements also set a more strategic approach, particularly from product diversification needs, cost optimisation, brand recognition and loyalty, sustainability initiative, and innovation.

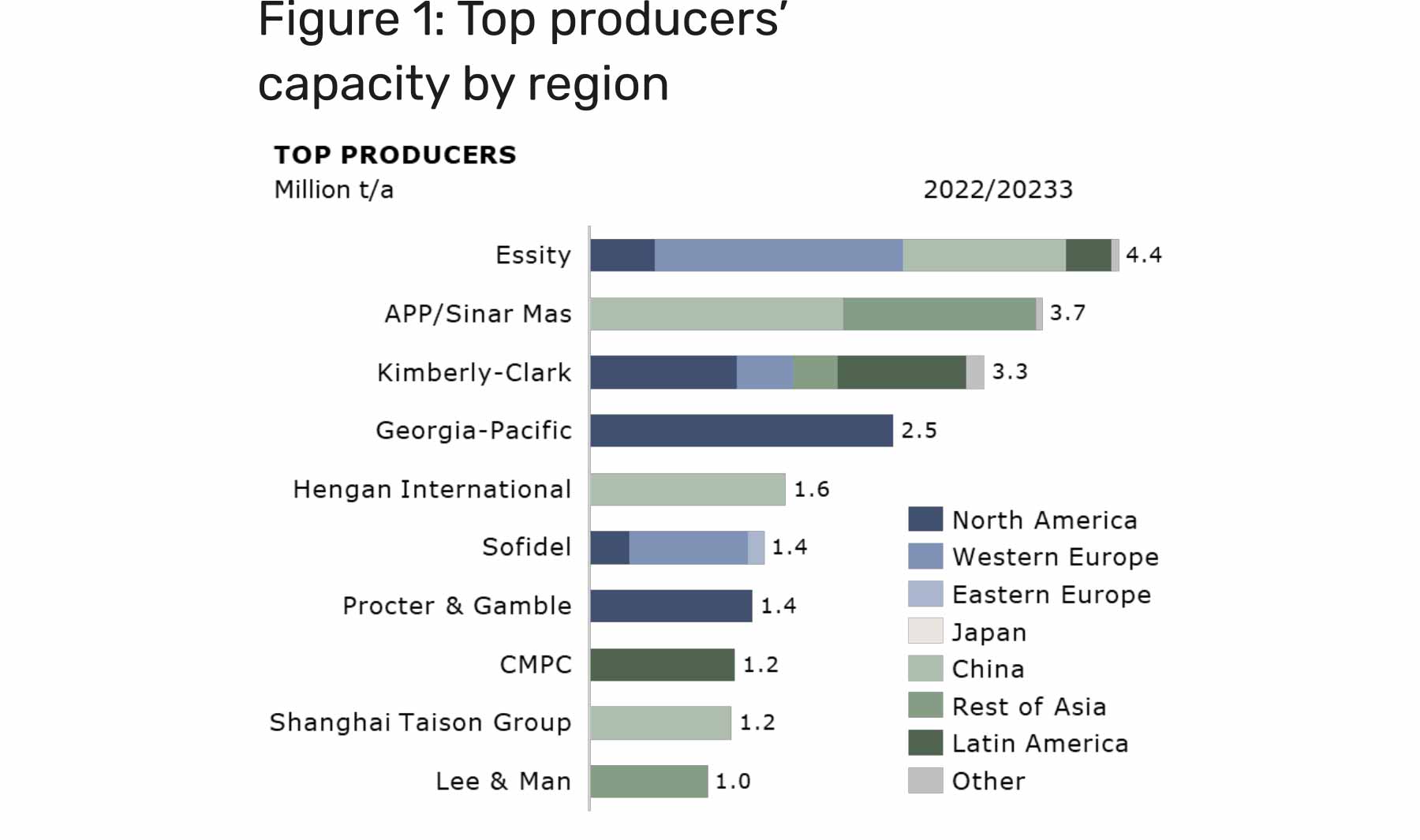

We start with where the production is by the top producers. As is evident except in a few cases, most producers are very regional. It is back to their approach to maximise the vertical integration to reap efficiencies and cost competitiveness. Also, most of the producers are in the region with access to raw materials and a large demand of tissue paper. On the other hand, for some producers with higher integration it brings more challenges in terms of global growth.

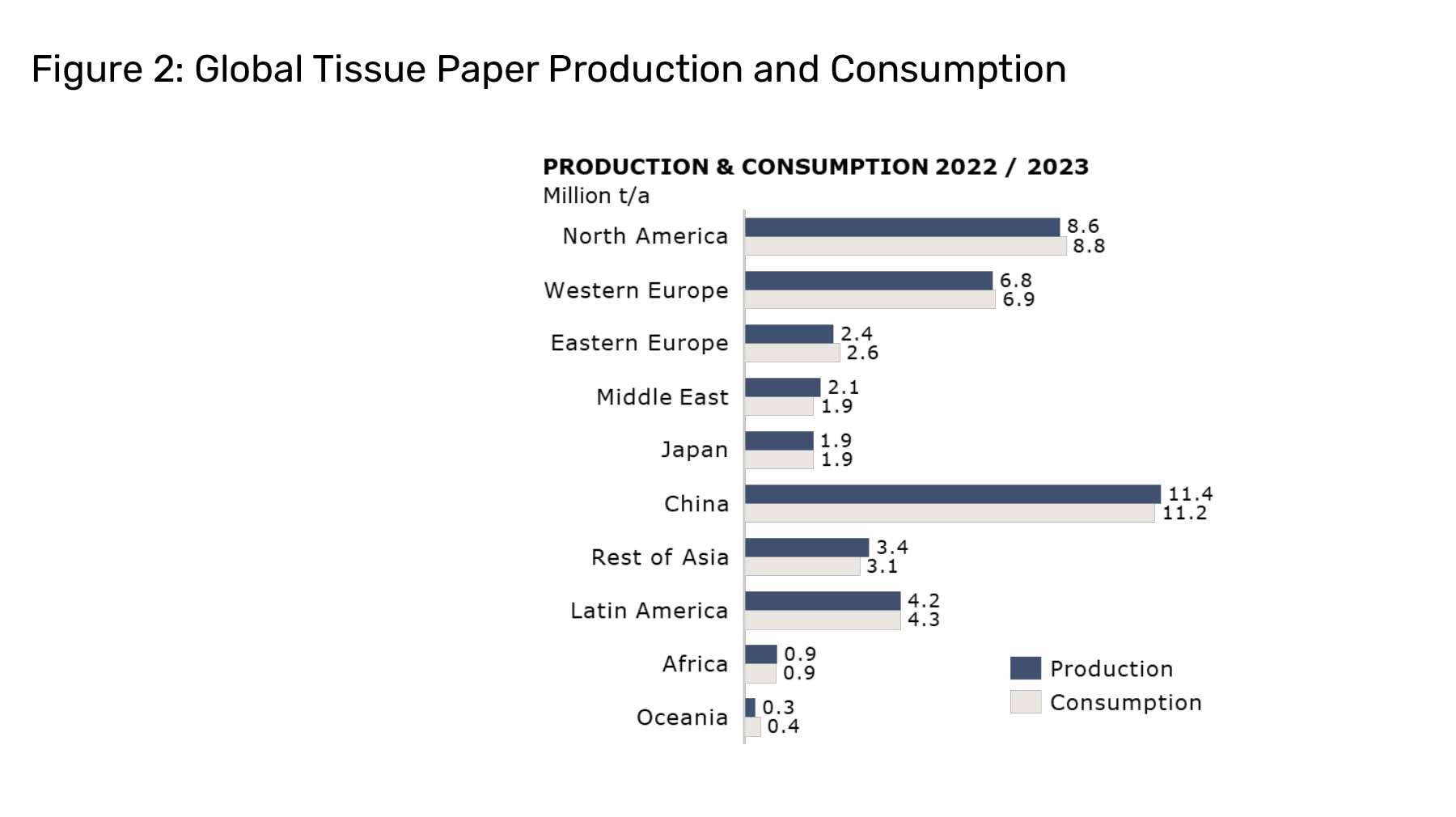

Next, pairing the tissue paper production and consumption, our argument that tissue paper is produced where it is consumed is further enforced. Since the early 2000s, developing and emerging economies have begun to significantly contribute to global volume growth, accounting for over 80% of growth over the past decade, with total global tissue consumption increased to be 41.9 Mt (2022).

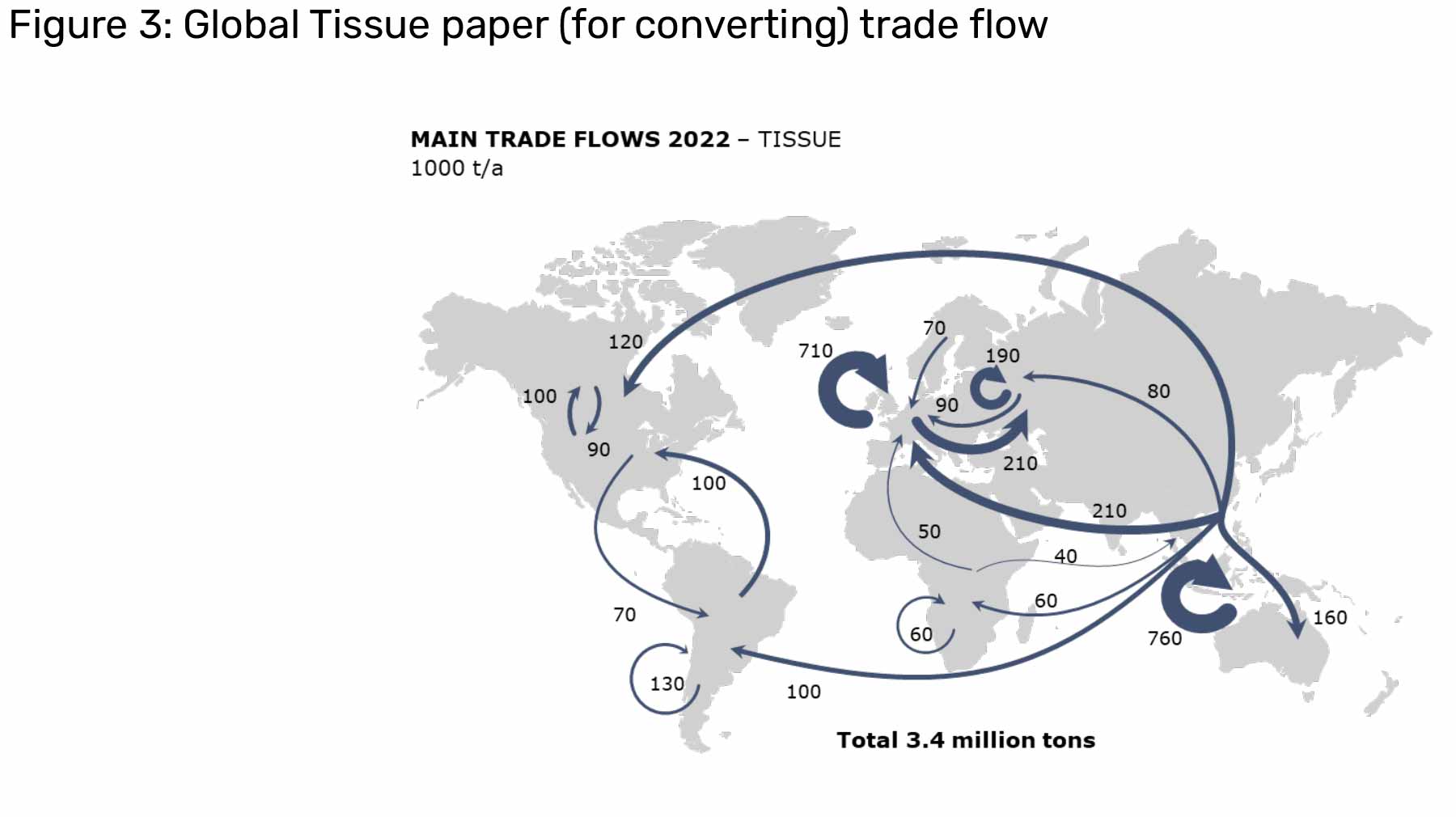

However, out of the 41.9m tons of tissue consumption, 3.4m tons are traded globally to be further converted locally in the destination market. This is sizable trade with majority traded with closely related regions, driven by the logistics cost and specific consumer requirements of inter-related markets. This is evident in case of Europe and Asian regions with sizable volumes being traded within the regions.

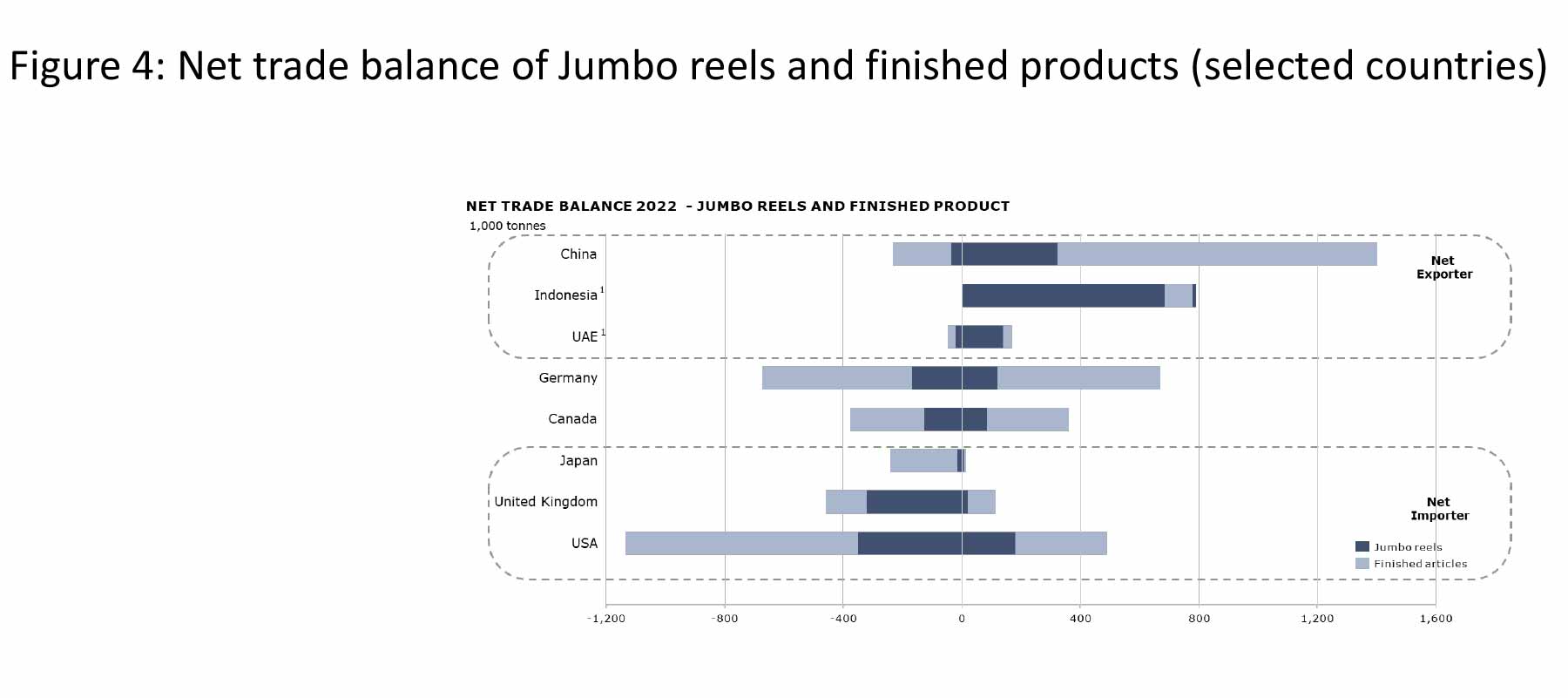

Next, when we look further across some selected countries comparing the trade of jumbo reels and finished products, there were some interesting revelations. Certain countries, for example China and Indonesia, are a net exporter of both jumbo reels and finished products. China was the biggest outlier with more finished products being exported, while the USA on the other end is a net importer of finished products. This is again a substantial volume with possibilities to trigger some scrutiny. This is again mostly absorbed by the continued move to private label (PL), as compared to branded tissue finished products. PL in North America is historically not as strong as in Europe. Furthermore, this trend of PL focused players is becoming bigger in the USA, while players with the big brands are becoming fewer, causing more disruption. Similarly, in case of Indonesia, the dominant trade flow is for jumbo reels which are being further converted in other regions, likely to bring scrutiny from the local market regulators.

In conclusion, in case of very selected few countries, there is a dominance of more finished products being exported either through traditional supply channels or e-commerce portals. Also, these are the ones that more exposed to geopolitical risks. This is an interesting market situation to note and is very contrary to the usual thinking related with tissue paper market models. Additionally, it supports the concern on tariffs from some of the producers that we interacted with.

This situation will intensify when the additional capacities come online in Asia by 2030 and they also start looking for more export markets for both jumbo reels and finished products. An interesting market. However, it remains to be seen how far this impact is going to happen and to which segments. Definitely a topic of discussion for another field trip.