The pandemic meant record sales for retailers. But beyond external market demand spikes and input cost deflation, strategic and operational planning led to top EBITDA performance. Sanna Sosa, Senior Principal, and Sivashankari Bharathi, Analyst, AFRY, explore the intrinsic and longer-term drivers.

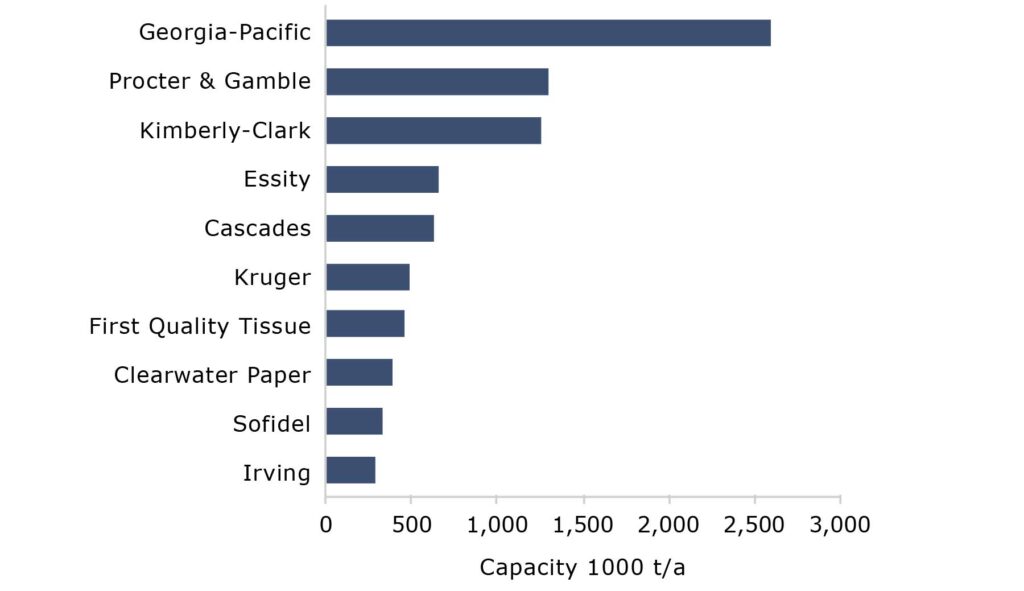

The North American tissue manufacturing landscape consists of about 20 companies. The top 10 largest tissue product manufacturers represent 90% of the total industry capacity [Figure 1]. Out of the top 10 tissue companies, five – Procter & Gamble (P&G), Kimberly-Clark (K-C), Cascades, Kruger and Clearwater – are public companies and offer visibility into their tissue business performance. We will focus our lens on these five companies, their EBITDA performance and differences in strategic approaches and operating models.

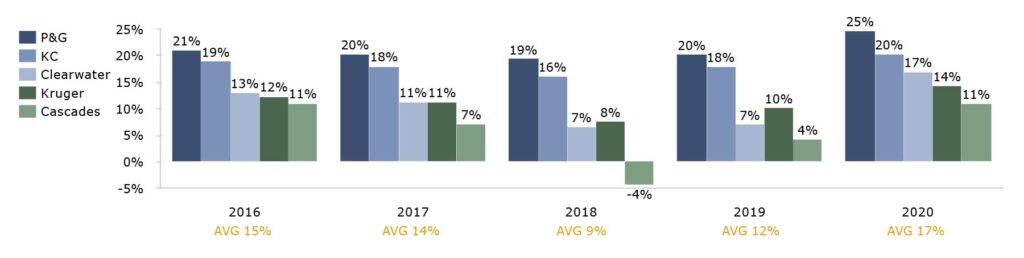

In 2020, tissue companies’ EBITDA margins increased to the highest level during the past five years [Figure 2]. P&G’s tissue business has consistently had the highest EBITDA performance against its peers at about 20% or above. K-C is the next best performer with tissue business EBITDA steadily above 15%. Clearwater, Kruger, and Cascades have all had their EBITDAs mainly under the 15% threshold, dipping sometimes even in single digits.

Fundamental strategic decisions

As we try to understand which company strategic and operational choices are more conductive to higher performance, let’s start with some of the most fundamental strategic decisions for any company: in which businesses and markets to participate, i.e. diversification; in which product market segments to position its products, and how to grow [Table 1].

Diversification

Tissue companies are typically either diversified across other consumer and healthcare products (e.g., diapers, razors, skin and personal care products) or other pulp and paper products (e.g., containerboard, cartonboard packaging). The top EBITDA performers P&G and K-C are diversified in the consumer and healthcare product segments. Both also see lower variability in their tissue business EBITDA margins, compared to their other pulp and paper sector diversified peers. As Covid-19 cases fluctuated throughout the year, consumers began hoarding household cleaning and disinfectant wipes. Manufacturers were not prepared for the sudden increase in demand for wipes and began working “around-the-clock” to supply consumers, who emptied the shelves within the restocking hour. K-C, which reported a decline in its AfH segment sales overall, announced that sales for wipers increased by double digits in North America. Many companies have also been investing in their nonwovens segment. K-C reported investing nearly $140m at its nonwovens manufacturing site to expand capacity, while Georgia-Pacific (GP) recently announced the sale of its nonwovens business to Glatfelter for $175m.

Tissue companies are typically either diversified across other consumer and healthcare products (e.g., diapers, razors, skin and personal care products) or other pulp and paper products (e.g., containerboard, cartonboard packaging). The top EBITDA performers P&G and K-C are diversified in the consumer and healthcare product segments. Both also see lower variability in their tissue business EBITDA margins, compared to their other pulp and paper sector diversified peers. As Covid-19 cases fluctuated throughout the year, consumers began hoarding household cleaning and disinfectant wipes. Manufacturers were not prepared for the sudden increase in demand for wipes and began working “around-the-clock” to supply consumers, who emptied the shelves within the restocking hour. K-C, which reported a decline in its AfH segment sales overall, announced that sales for wipers increased by double digits in North America. Many companies have also been investing in their nonwovens segment. K-C reported investing nearly $140m at its nonwovens manufacturing site to expand capacity, while Georgia-Pacific (GP) recently announced the sale of its nonwovens business to Glatfelter for $175m.

The North American tissue market consists roughly of a 70% steady demand for the At-Home tissue segment and 30% of a more cyclical AfH tissue segment. Except for P&G, the four other public tissue companies are all diversified across At-Home and AfH products. Looking at some of the other top tissue players in North America, Sofidel, Irving, and GP are similarly diversified across both At-Home and AfH tissue product markets. Of the top tissue players, only Essity in North America and First Quality are concentrated in just the one segment, AfH and At-Home tissue and hygiene products respectively.

Target product segments

The highest performing tissue company P&G solely manufactures and markets branded tissue products, while at the other end of the spectrum Clearwater manufactures only private label products. The three other companies in focus manufacture both branded and private label products. However, K-C, the second-highest performer, only allocates a small percentage (estimated around 5%) of its retail tissue capacity towards private label products. While private label products have been gaining market share, branded tissue products still typically command a 25% or higher price premium in bath tissue and 40% or higher price premium in towels over private label products. Hence, it is easy to understand the higher overall business profitability of the branded players. Brands continue to offer competitive advantage, sometimes referred to as a moat. Of course, creating strong consumer brands has taken decades of marketing effort and investment to create, and are best managed by companies with consumer products and marketing business focus and DNA.

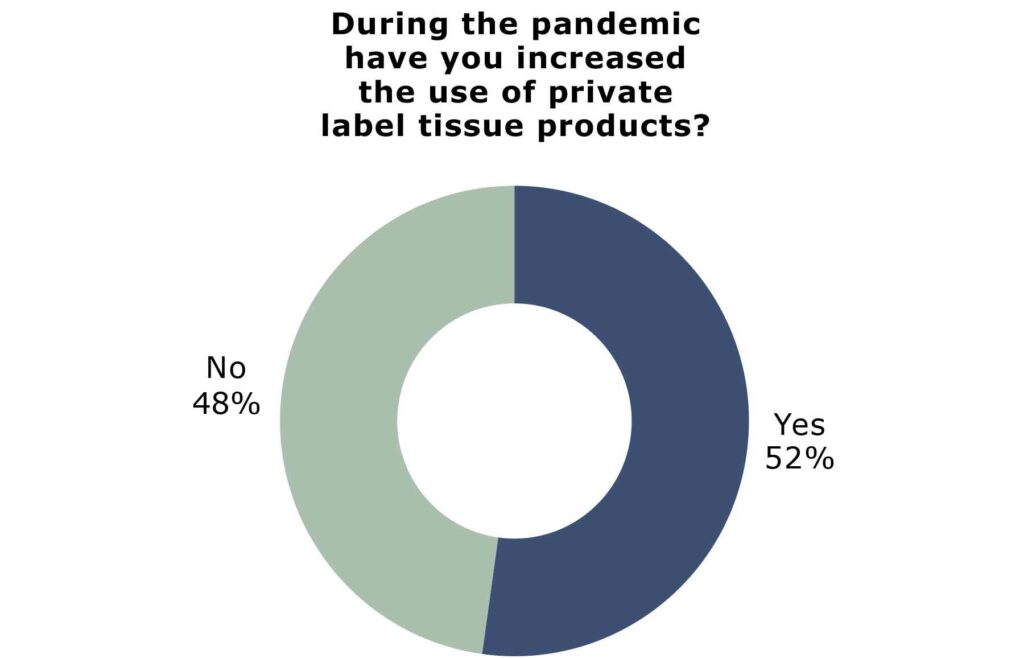

However, private label’s market share has been steadily growing. In 2020, at the onset of the pandemic, more consumers got familiar with private label tissue products when the store shelves were empty of their regular brands. And those experiences with tissue private label products were often positive and many consumers have reported willingness to increase their use of private label tissue products, hence supporting further growth of the private label market segment [Figure 3].

The North American tissue market is not only very brand oriented, it is also very quality oriented. With consumers actively looking for higher quality ultra-premium products, companies have invested in new ultra-premium quality TAD machines. Measured by the type of installed manufacturing capacity, the highest quality producing TAD technology represents almost 50% of the total North American retail tissue capacity. P&G and K-C both have TAD capacity shares at or above 50%, with P&G having 100% of its capacity TAD machines. Clearwater, Kruger, and Cascades have much lower TAD capacity shares. Kruger has been growing its ultra-premium capacity by investing in TAD machines in the upcoming capacity at Sherbrooke, QC.

Growth

Although P&G has been active on the M&A front in its other consumer products, it has not had tissue business M&A or machine capacity growth in North America since a greenfield tissue mill investment in Box Elder, UT, in 2015. K-C has been working on its global restructuring programme, aimed to reduce its global workforce by 12% and close around ten production sites to improve costs. The restructuring programme included the closure of its Fullerton, CA, mill site in 2020, with machine replacement and investment programs in Jenks, OH, and Mobile, AL, although with net zero impact on K-C’s total tissue manufacturing capacity.

North American tissue growth has been driven by the medium size players. The medium size, privately owned Sofidel and First Quality have been tissue capacity growth leaders. Clearwater and Kruger, in recent years, have also increased their tissue capacity. In 2019, Clearwater installed a new PM at its Shelby, NC, facility producing 65,000tpy of tissue.

In 2017, Kruger installed a second-hand PM at its Crabtree, QC, facility and brought a new 70,000tpy TAD machine online in the first quarter of 2021 to supply ultra-premium bath and paper towel tissue at Sherbrook. In early 2021, Kruger announced it would continue with its $240m expansion plan at Sherbrook by adding a 30,000tpy light dry crepe (LDC) tissue machine and two converting lines over the next three years.

On the inorganic growth front, Cascades acquired Orchids Paper in 2019, growing its tissue capacity by nearly 90,000tpy. Cascades has also recently shut down 60,000tpy of aging, low profitability capacity at Ransom, PA, and rationalised its converting footprint. Cascades reported that the closure is a part of its ongoing strategic initiatives to improve its tissue business’s profitability.

Companies’ operational approaches

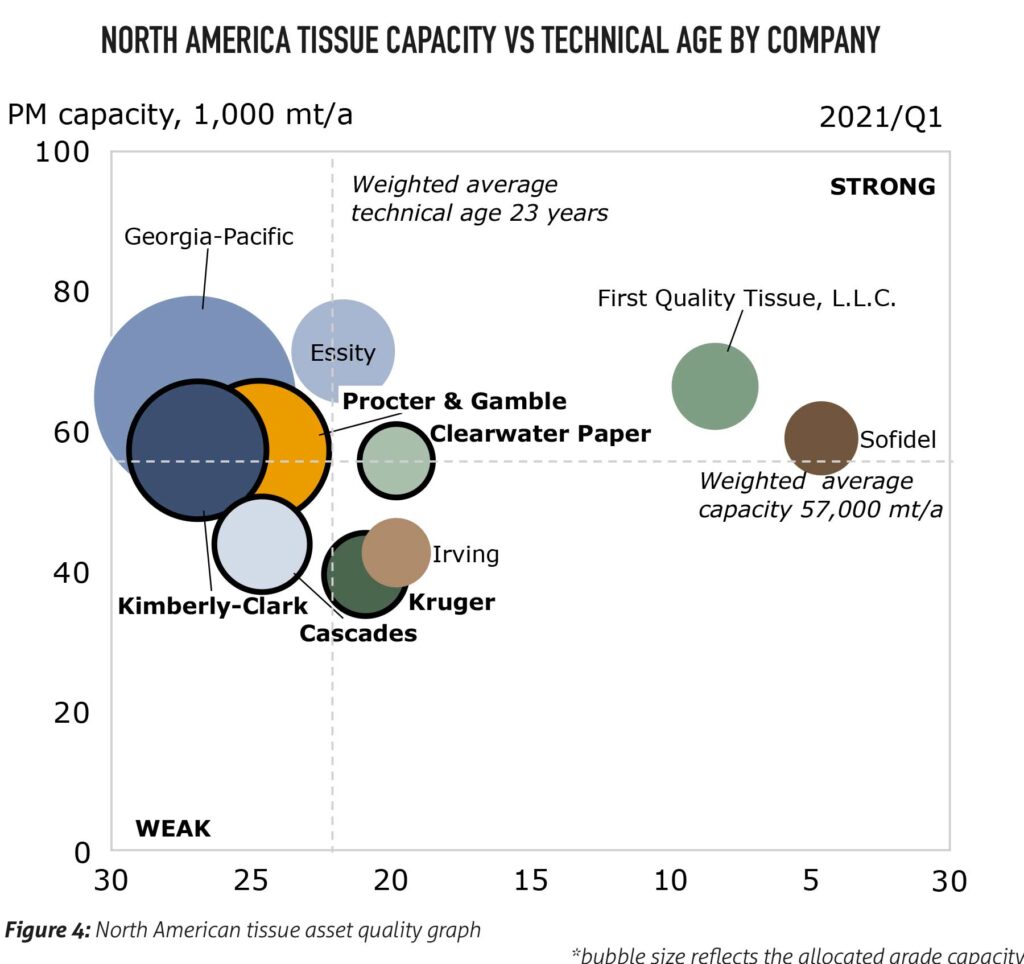

North American tissue companies have a variety of operations approaches when it comes to scale and technical age, i.e. asset quality, of their tissue manufacturing footprint as well as integration – both forward integration to converting of tissue products, as well as backward integration to fibre raw material.

Asset quality

Our asset quality chart [Figure 3] illustrates how the investments made by the

medium size players such as Clearwater, Kruger, Sofidel, First Quality, have made their asset footprints amongst the most modern tissue manufacturing platforms in North America. The high performing incumbent tissue giants still tend to have larger machines producing their large manufacturing run branded tissue products than the medium size companies, although the medium size tissue companies have started to close the gap by installing larger scale tissue machines.

Integration

Tissue manufacturing is typically forward integrated into converting of the final products, but un-integrated into fibre, meaning highly reliant on market pulp. Most tissue products are converted on-site, at the tissue mills, to save on costs. Off-site converting is another operations configuration employed, but to lesser extent. Companies such as Cascades has recently been rationalising its converting footprint by closing three off-site converting facilities within the last year to optimise its tissue business’ operational efficiency.

Fibre costs can represent 40-60% of jumbo roll tissue manufacturing costs, which makes tissue company EBITDAs highly sensitive to fluctuation in fibre costs, whether recycled fibre or market pulp. Based on AFRY estimates, only about one quarter of retail tissue products in North America are made with integrated pulp. Backward integration of tissue manufacturing has been a growing trend globally, whether through forward integrating market pulp operations and co-locating tissue assets at, or adjacent, to partner companies’ pulp mills.

Performance during and beyond Covid

During the pandemic, the tissue industry regained its recognition as an essential industry and returned to higher profitability driven by the spike in demand and depreciation in fibre costs.

Focus on the premium product quality branded tissue market segment seems to still be the driver for highest margins, due to its continued ability to command a premium price. Yet, tissue companies have turned into asset footprint rationalisation and restructuring programmes to improve EBITDA performance from the cost side.

The large At-Home, brand-oriented tissue companies still have a clear margin advantage to their smaller, private label-oriented competitors. The growth of medium-size companies will also challenge the incumbents with their modern manufacturing assets and focus on the continuously expanding private label market.