After unprecedented turbulence in world economics, the industry – focussed on Europe – has shown “broad margin improvement.” AFRY Management Consulting’s Hampus Mörner, Manager, Christoph Euringer, Senior Principal, and Tino Mäkelä, Consultant, examine the evidence.

Every year since the beginning of this decade has brought surprises and unexpected events resulting in persistent volatility for the global tissue markets. This volatility, never seen before, first manifested in hoarding, followed by collapsing AfH demand, occasionally soaring energy and fibre costs, shifting consumer behaviour, depressed consumption, and intensified competition.

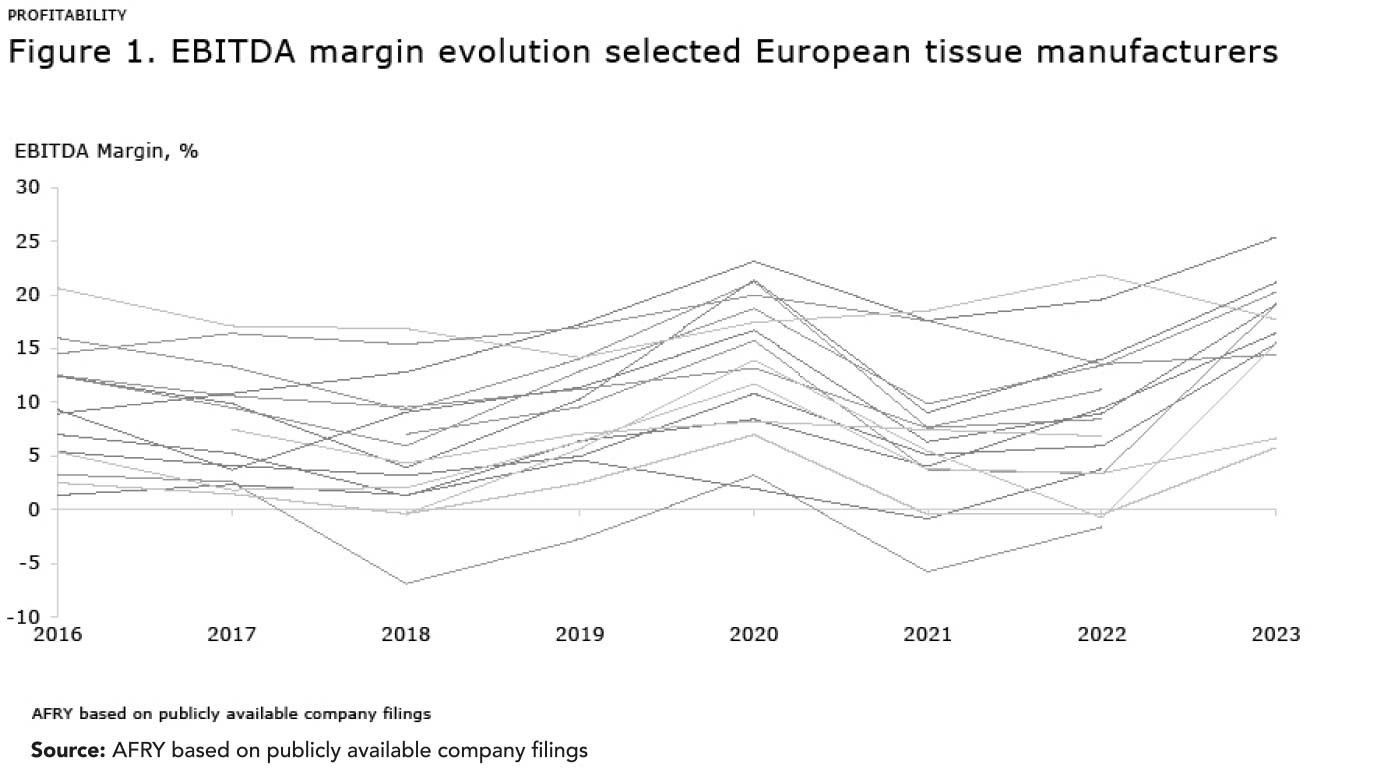

At first glance, an instant reflection might be that tissue industry is on its way to a critical turning point. In fact, data suggests that it has navigated this turbulent environment very strongly, and seems to be in solid shape.

Figure 1 illustrates the evolution of EBITDA margin for a significant amount of tissue producers in Europe. Taking from this, there is little that would suggest that the industry is heading to any critical point – rather the opposite, in fact – a broad margin improvement was observed during the last year. So, what are the key events that the industry seems to have tackled so well, and what learnings and reflections can be done moving forward?

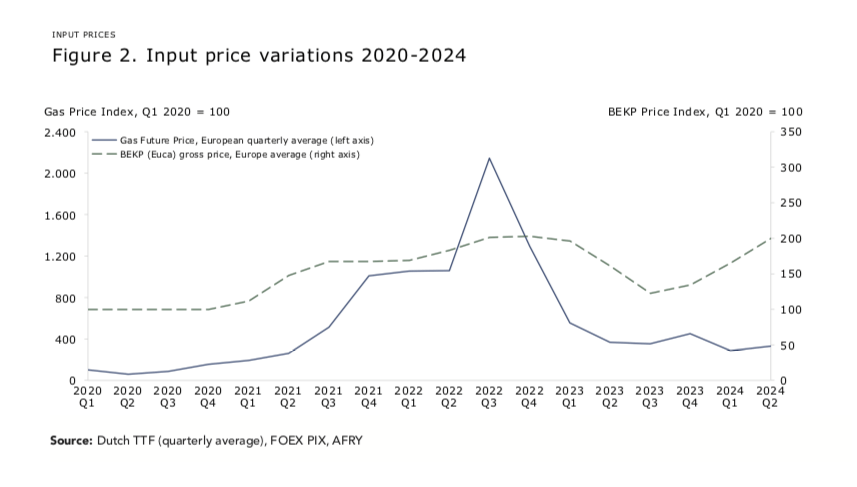

Volatile energy and fibre costs: Energy and fibre are the most crucial inputs when producing any paper product, and their cost development has been on a rollercoaster ride. As an example, German and Italian gas prices were up by 160 – 450% respectively in 2022 (year-on-year). At the end of 2022 energy price outlooks were sky high and a significant burden for any energy intensive industry, but, luckily, prices started to come down in early 2023. Although long term price outlooks point towards a more stable situation than two years ago, there are many uncertain factors.

While energy prices were exposed to an unseen dynamic, pulp is a cyclical commodity. For virgin fibre pulp, publicly listed gross price indices were at rock bottom when the pandemic started in early 2020. Like other commodities, it remained low and flat throughout most of the year only to surge when economies and supply chains sparked up in early 2021. Since then, consecutive ‘all time high’ levels have been registered with a few short breathing moments e.g. H2 2023. If putting the last year’s price movements in a longer historic context, it is apparent that pulp prices have become more volatile where cycles tend to be steeper and shorter.

It is worth noting that price discounts have continued trending upwards. A significant factor fuelling this volatility is China’s expanding presence as a pulp end-use market, currently accounting for over 40% of global demand. Moreover, market dynamics in this region diverge significantly from those in the Western world, e.g. more speculative buying, shorter contract periods, recurring negotiations and aggressive inventory management, with less focus on working capital.

Changing consumer behaviour and demand recovery: Inflation above the target of 2% in most countries has been the default for the last three years. A result of disrupted supply chains and rising energy prices due to geopolitical events. With reduced spending power, consumers tend to think twice about what finally goes into their shopping basket.

Of course, articles considered ‘a must have’ enjoy some protection (e.g. toilet paper) that other articles do not (e.g. napkins). The market has observed continuously raised penetration of private label in consumer tissue. Still it has not been growing above trend or perhaps as strongly as many would have expected despite the inflationary pressure which is now coming down. This indicates that brand loyalty has stood up well against inflation.

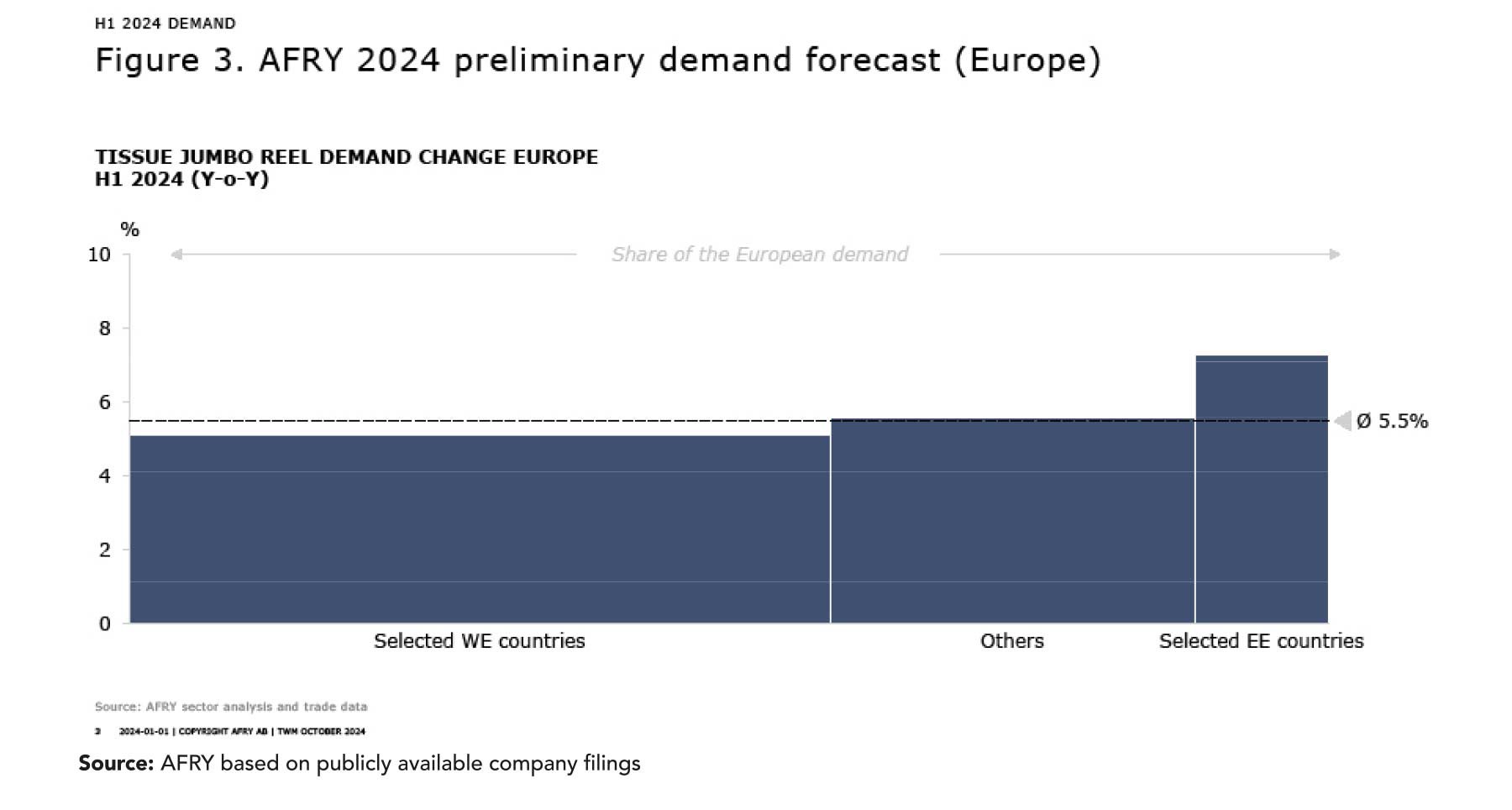

While overall consumption of tissue decreased in 2023, actual consumption data for the first half of 2024 already indicates a broad recovery in total demand of ~5.5% (Figure 3), owing much to the AfH segment.

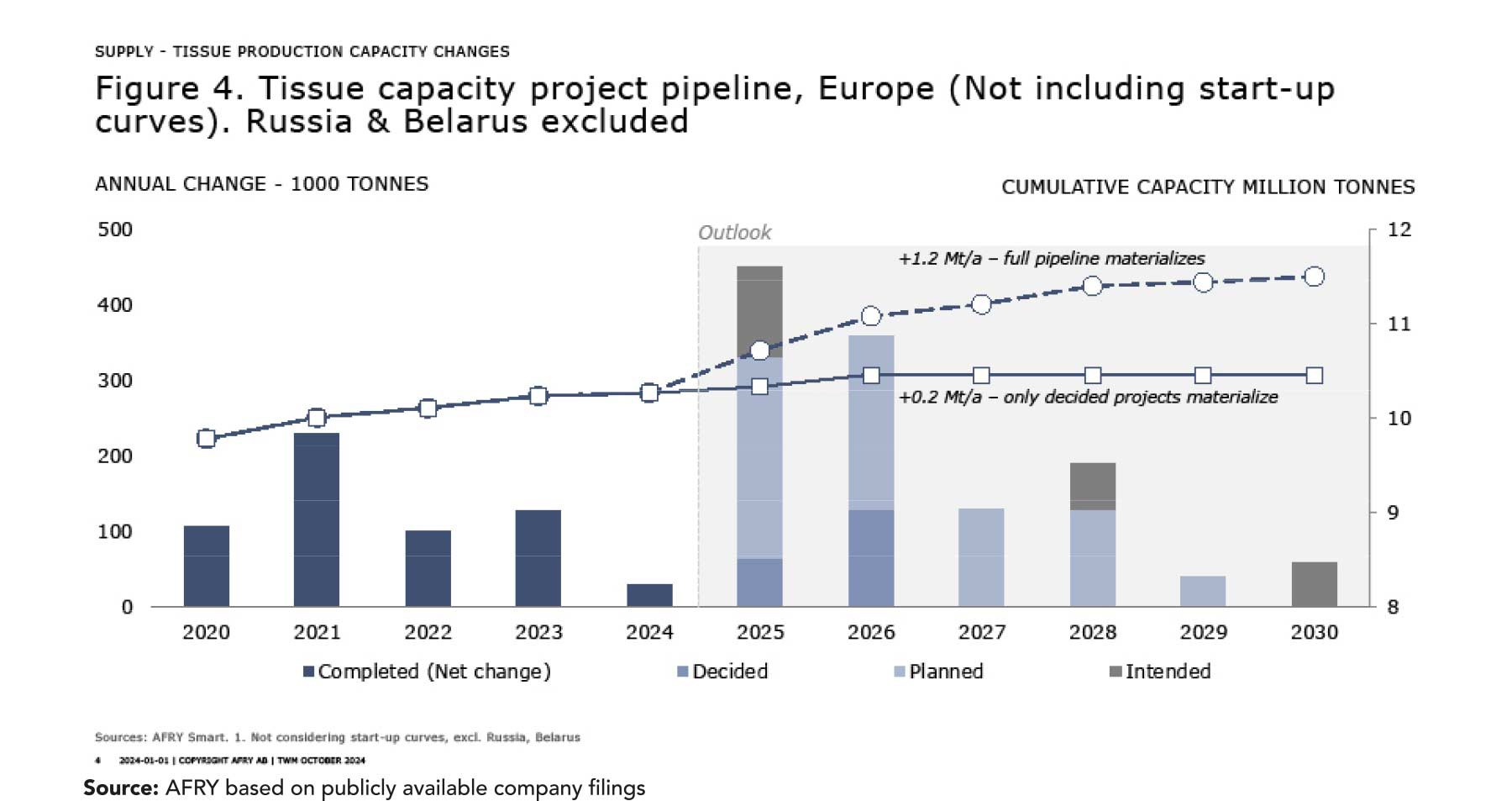

Notable tissue capacity pipeline: For any outside observer there would appear to be a massive project pipeline of new tissue capacity in Europe, which to some extent is correct. Currently there are numerous projects announced totalling over 1.2m tonnes of capacity of which many are to be found in Western Europe, and in particular the UK and France. However, a closer look reveals that numerous projects are still short of a formal investment decision (Figure 4). About 200,000 tonnes of new capacity is currently decided, while around 1m tonnes belong to any of the categories still to be confirmed (planned and intended).

Current supply and demand can be considered balanced, but a hasty entry or an overabundance of projects materialising could easily destabilise markets. What is clear is that the continent seems to be moving more towards self-sufficiency and that finding room for volumes originating from the outside may become more challenging. Still, there is a sizeable amount of cost-efficient capacity with established routes into Europe, ready to take on the competition. Regardless of where the production will take place, the importance of cost competitiveness will only increase.

Future competitiveness will be built on multiple pillars and being cost efficient is key, but is not the only important factor.

For institutional buyers as well as retailers, the sustainability impact of tissue becomes more relevant – for their own reporting needs – due to new legislation on green claims, but also to satisfy their own brand building efforts.

Furthermore, as the decarbonisation of the European energy system is progressing and machinery suppliers are providing multi-fuel and fully electric tissue machines, the bar is about to rise.

Shifting the buying criteria of customers – not necessarily yet the consumers – is about to create an actual competitive advantage for the European industry, and from the mid to long term perspective, this may well protect European producers from low-cost imports that may benefit from lower sustainability standards in fibre, health and safety, or fuel choices.