Dominant private label, high energy costs, influential NGOs, an ageing population… Metsä Tissue outlines its way forward in a challenging German market. Tissue World editor Helen Morris meets Christoph Zeiler, Metsä Tissue’s senior vice president, tissue, western Europe.

It isn’t long after meeting the very friendly Christoph Zeiler at Metsä Tissue’s Raubach mill in Rhineland-Palatinate that the free-flowing conversation – as his English is excellent – gets round to the ‘elephant in the room.’

This elephant, unlike the cliché, isn’t being ignored, far from it. We usher it in, give it a sugar cube and look it straight in the eye: the dominance of private label in the German market – a phenomenal 78% of tissue sales in 2012 compared to 45% in the UK and 20% in the US.

Across such a marketplace, providing a point of difference is vital and in many aspects the private label monopoly has obliged many tissue companies to look outside the box in terms of innovation and market strategy.

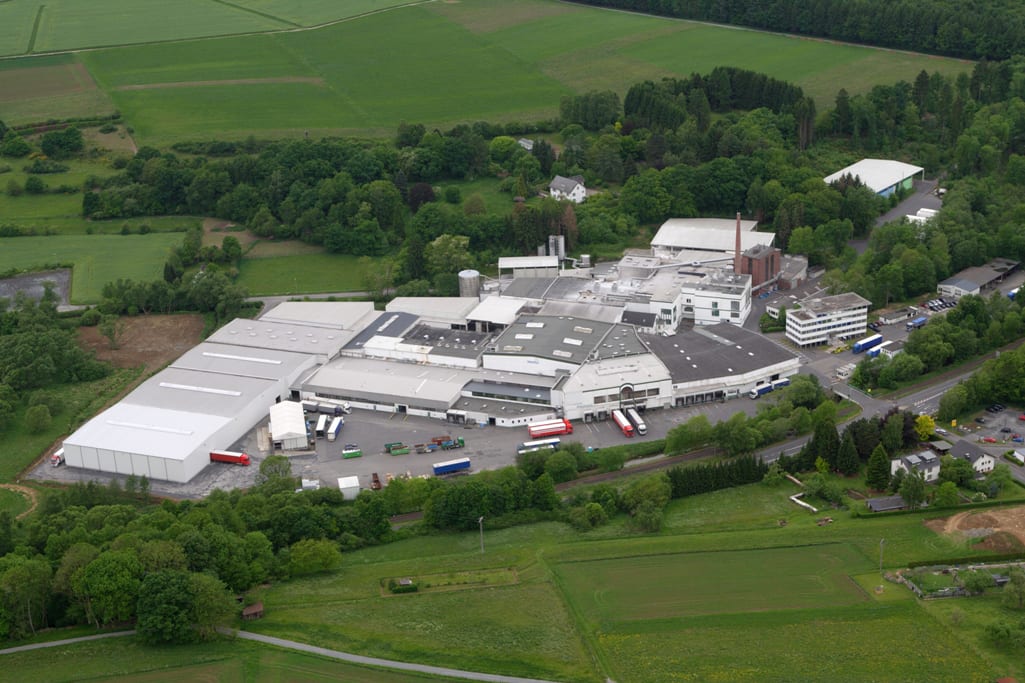

The mill houses two PMs as well as nine rewinders, converting 75,000tpy of AfH and consumer products. Metsä Tissue has three tissue mills in Germany with a total tissue capacity of 250,000tpy, with the other two mills producing products for the consumer and speciality napkin markets. Walking around the plant, Zeiler elaborates on how the private label market dominance means the business has to be a cost leader. “We develop and innovate, but for us innovation doesn’t always mean product development,” he says. “We look at machinery investment or energy efficiencies … at the Raubach site for example, we are in the process of completing a paper machine upgrade with Toscotec that will clearly improve the site’s energy efficiencies as well as increase our capacity.”

‘Energy costs are critical to us and the whole of the tissue market and there is a high risk that they will explode.’ Christoph Zeiler, Metsä Tissue senior vice president

He adds that energy consumption is one of the biggest issues the industry has in Germany. “These costs are critical to us and the whole of the tissue market and there is a high risk that energy costs will explode,” he says. “We reduced our energy use company-wide by 20% between 2007 and 2012 and by 2020 we’re aiming to improve our energy efficiencies by a further 10%. In this field of business energy issues are important to us both from cost structure and sustainable points of view. Even if we focus on developing our energy efficiency continuously, we’ll need reasonable cost level energy also in the future.”

The company is looking to grow organically in the European markets and Zeiler adds that this is challenging in a market that has seen a flat 1% growth over the past few years. Consumption in Germany is growing only very slightly, he says, but it is still growing, and this is one of the biggest issues for the business: “We have plenty of players in the German tissue market but demand is fairly flat. And again, this is especially the case where private label is so dominant.”

It is vital that the industry looks to increase consumption such as introducing novelties that fit well into their customer’s every day life. “Per capita consumption in European countries varies. For example, consumption in Switzerland and in the UK is higher, while in Poland consumption is a little bit over seven kilos per person per year. Consumption in Germany is above the average European level, but there’s a clear possibility for growth in comparison with the UK and the USA.”

“We are certainly looking at organic growth, this is a big focus for us and requires some investment.” In Metsä Tissue’s Krapkowice mill in Poland, the company recently finalised a €55m investment to build two paper machines, a new AfH product converting line as well as extending the converting and warehousing facilities. “It has made it more energy efficient too,” he adds. “We want to grow above market growth there and in Germany, and innovation and organic growth are key to achieving that.”

Growth will also take place through exports and the company is also doing some business into bordering countries as well as the UK, Ireland and as far south as Italy. “We want to produce as closely as possible to our customer base, because the further away we are the more expensive the product gets,” Zeiler says.

Green investments continue to be a factor that boosts the German tissue industry and most companies and brands as well as private label manufacturers offer at least one green product. This year, the retail value share of recycled toilet paper is 8%, but its share of sales has fallen from the 10% it held five years ago. At the same time the recovered fibre availability has turned to clear decline due to media digitalisation. As sustainability is a leading issue, our understanding about the environmental footprints of different fibres is deep. It’s a surprise for many that the recovered and virgin fibres are quite equal from their environmental point of view in tissue production.”

‘There are always challenges and there will be more to come. Today’s are different from the last economic downturns.’

However, economic concerns don’t appear to have impacted German consumers’ desire for sustainable products and green continues to be a way for the market to offer value. Zeiler says: “We have been one of the first having all kinds of environmental, energy and work safety related certifications but we need to keep going with innovations too in order to develop the business.”

The German market, he says, is continually under pressure from campaigning NGO’s. “They have significant influence over the retailers. Their pressure passes down to the retailers, it is the NGOs that are defining the name of the game in terms of products and sustainability. We’ve been dealing with this for many years and reacting. We can help to deliver safe products and we directly cooperate with the NGOs. It’s getting more challenging and demanding but there are solutions.”

Following the trends and the brands is one option, but he adds: “I hope the brands grow here because in turn they are helping the entire sector to grow. Brands have around 10/15% of the German market and it is very important to develop this. It is difficult to get new brands into this marketplace but as producers, this doesn’t mean that private label producers are less innovative.”

‘In Germany, we don’t just see the local economy, we see Europe as a total. We are moving towards a better direction.’

Is the current climate more severe than what he’s experienced in the past? “There are always challenges and there will be more to come. Today’s are different from the last economic downturns. In Germany, we don’t just see the local economy, we see Europe as a total. We are moving towards a better direction. It is steady and developing away from the recession and towards calmer waters. But we remain with countries with weaker economies such as Greece… and that is a big challenge for us to develop.”

The tissue market’s product groups have also “not been so severely impacted on by the recession”. “Tissue has done OK because it is needed on an every day basis here, regardless of the recession. AfH is one of the only tissue areas with a direct connection to the economy and it has been the one to suffer the most. But generally, tissue isn’t recession sensitive.”

Germany’s rapidly ageing population and low birth rates have impacted on demand. “The ageing population here has an indirect impact on tissue. It’s very important and means we have to finance a range of options. There are no simple solutions on the table and it is a big challenge. But the future is looking positive. There is room to grow and innovate but it’s up to us to be active.”