NBSK pulp Europe

NBSK pulp Europe

NBSK pulp Europe

NBSK pulp EuropeThe consumption of softwood pulp was down and inventories up in October in Europe, compared to both September 2015 and October 2014, as reported by UTIPULP. The narrow price gap between softwood and hardwood pulp may be already helping NBSK supply/demand balance globally but much of that support is not seen in Europe, at least not towards the end of November.

Global statistics are not available at the time of writing these notes but suppliers of softwood pulp report in most cases low inventories.

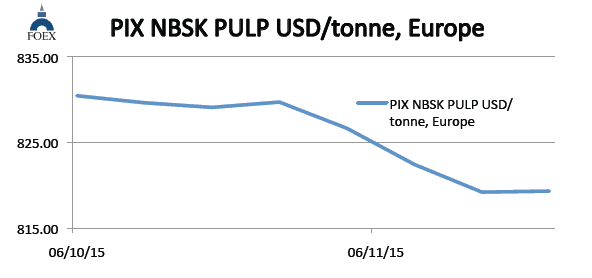

On the supply side, the re-start of the bigger recovery boiler at Pöls is approaching. Gradual price erosion seen over late October and the first week of November, coinciding with the strengthening of the US dollar, came to an end, at least temporarily in week 47. Our PIX NBSK index value in dollars came up this time by 12 cents, or by 0.01%, and closed at 819.31 USD/tonne.

US dollar strengthened against the Euro by 0.5% (weekly average). With the strengthening of the US dollar against the Euro, the benchmark value in euro, converted from the dollar-value index with the average exchange rate of last week, headed again clearly higher, this time by 3.82 euros, or by 0.50%, and the PIX NBSK index value in euro-terms ended at 766.64 EUR/tonne, only 1.5 euros lower than in the beginning of the year.

BHK pulp Europe

The hardwood pulp numbers were again not available from UTIPULP when updating these notes. The weakness of the Chinese market radiates also elsewhere in the world, including Europe. On the supply side, the list of production disturbances is long and some of the stoppages appear to last longer than first expected. With the El Niño phenomenon likely to strengthen further in 2016, the climate-related disturbances risk continuing into next year. The total loss of over 300,000 tonnes mentioned in the press appears to be correct. It does include, however, also normal annual maintenance downtime, i.e. tonnage which would in any case not have been produced during the fourth quarter, even if the precise timing might have been different.

With the near-term views of the producers and consumers quite far apart, prices continue to ease lower. Our BHKP benchmark in Europe eased lower again, slightly more than NBSKP, by 1.38 dollars per tonne, or by 0.17%, and closed at 801.61 USD/tonne. In week 47, the value of Euro depreciated by 0.5% against the US dollar (weekly average). When converting the USD-value of the BHKP index into the weakened Euro, the PIX BHKP index in Euro moved up by 2.35 euro, or by 0.31%, and closed at 750.08 EUR/tonne, up by 140 euros from early January.

Paper industry

The first October data from the US is mixed. Corrugated box shipments were up, after adjustment to shipping days, by 1.6%, y-o-y, and inventories fell, but remained above the longer-term average. Compared to the beginning of the year, packaging sales have, however, slowed down in relation to the growing capacity. The Q3 financial results were weaker and some production downtime is being taken in November. Uncoated free sheet shipments were down in absolute terms but also marginally up, when taking the number of shipping days into account. Kraft papers were very strong with an over 7% increase in shipments over October 2014.

Box board data had been clearly weaker than containerboard data over the first 9 months of the year but October numbers were quite positive, especially for CUK, but SBS and Folding Boxboard numbers were positive as well.

In Europe, October paper and board data has not been published yet. Order books in graphic papers were, on average, quite good during the month but have weakened in most grades in November. The same applies to tissue where the third quarter and still October operating rates were quite good but some weakening has been detected in November. And tissue is typically less seasonal than most other grades of paper. In packaging, shipment volumes remain pretty good but the already seen capacity increases, and especially those approaching, cause concern. The prices of recycled paper based grades have slipped lower over the past couple of weeks.

About FOEX Indexes

FOEX Indexes Ltd produces audited and trade-mark registered PIX price indices for certain pulp, paper packaging board, recovered paper and wood based bioenergy/biomass grades. The PIX price indices serve the market in a number of ways. They function as independent market reference prices, showing the price trend of the products in question. FOEX sells the right to banks and financial institutions to use the PIX indices for commercial purposes, while RISI Inc. has the exclusive re-selling rights for subscriptions to the PIX data and market information. Please enquire for subscriptions at [email protected] or via the following link www.foex.fi/subscribe/

Tissue papers are produced either from virgin fibre, recovered fibre and various mixes of both, depending on the end product. High quality hygiene tissue products like medical tissue products, facial tissues, table napkins or other such household and sanitary products are often made exclusively or almost exclusively from virgin fibre pulp, whereas the share of recovered fibre typically increases in tissue products for a variety of end uses outside personal hygiene, such as kitchen towels or towels for garages or other such industrial production facilities etc. Providing PIX pulp price indices gives the paper producer and buyer insight in the price trends with a weekly frequency. PIX indices are used as market reference prices e.g.

– by banks or exchanges that offer price risk management services for pulp buyers and sellers

– by buyers and sellers of pulp or paper in their normal supply contracts

– companies who want to employ an independent market reference price for internal pricing (e.g. pulp mill – paper/paperboard mill, paperboard mill – box plant) through licensing the commercial use from FOEX.

In addition, our price indices are widely used in financial analysis, market research and other such needs by all kinds of parties linked directly or indirectly to forest product or wood-based bio-energy industries.

This way the companies have better tools to budget their cost or income structure and profitability, and may concentrate on their core businesses with less time spent on price negotiations, which tend to increase in these days as the planning span narrows in the wake of the short, quarterly business cycles and, nowadays, in most cases, monthly raw material pricing decisions.

Subscription – For access to the latest PIX Pulp and Paper index values and commentary, please subscribe to the “PIX Pulp and Paper Service” via the following link www.foex.fi/subscribe/